Dear Members,

We have released 31st Mar’24: Repco Home Finance Ltd (NSE Code – REPCOHOME) – Alpha/Alpha Plus stock for Mar’24. For details and other updates, please log into the website at the following link – http://katalystwealth.com/index.php/my-account/

Note: For any queries, mail us at [email protected]

Date: 31st Mar’24

CMP – 400.65 (BSE); 399.55 (NSE) Face Value – 10.00

Rating – Positive – 4% weightage (this is not an investment advice, refer rating interpretation)

Introduction

Repco Home Finance Limited (Repco) is a housing finance company (HFC) registered with National Housing Bank (NHB).

Repco was incorporated in May 2000 as a subsidiary of Repco Bank, a Government of India enterprise.

The current stake of the promoter is 37.13%.

At around CMP of 400, we like it for the following reasons:

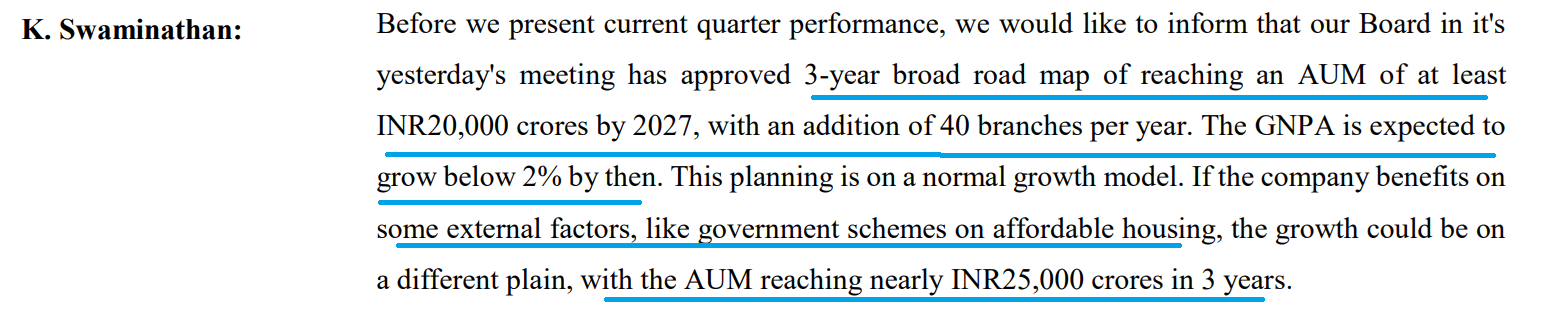

- Expect faster loan book growth – Between FY 20 to FY 23, company’s loan book grew only by 5% to Rs 12,449 crore. Going forward, on the back of set up of 200 + sales team and plans of addition of 40 branches per year, the management is targeting Rs 20,000 crore loan book by FY 27

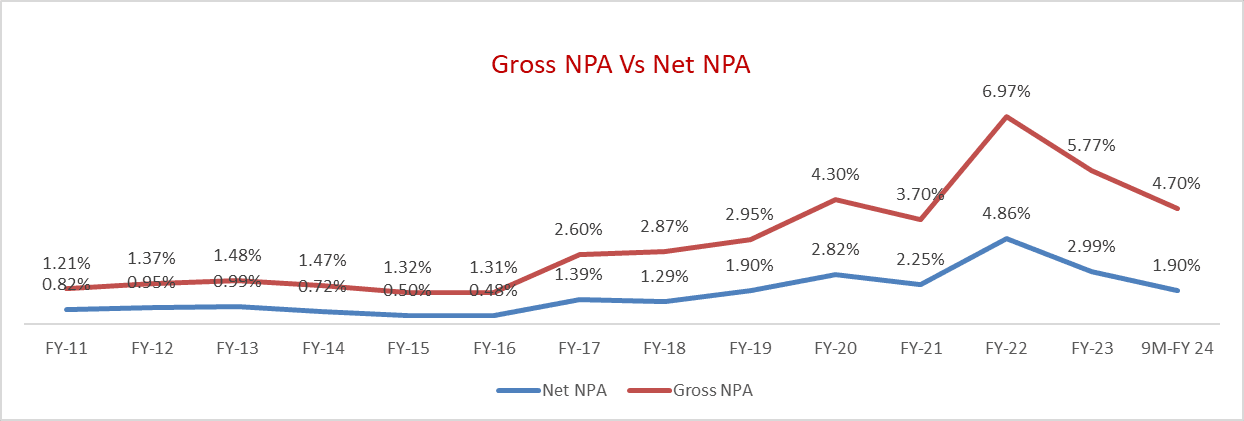

- Asset quality improvement – Due to pandemic, asset quality faced significant challenges, impacting cash flow in the non-salaried segment. As a result, the GNPA reached a peak of 7% in Q3FY22, accompanied by an SMA-2 (Special Mention Accounts) and restructured book exceeding 15% and 5%, respectively. Since then, GNPA has reduced to 4.70%, SMA-2 at around 12% and restructured book at around 4.1% in Q3 FY 24.

- Under new management, an internal 80 + people collections team was established, yielding positive outcomes

- Attractive Valuations – The stock is currently quoting at < 1 time book value and around 7 times TTM earnings. Company’s debt to equity ratio is only around 4. With expected credit growth pick up and improvement in asset quality, we believe there’s good scope for both earnings and valuations re-rating in the stock.

Business details

Repco is a housing finance company and focuses on Tier II, III, and IV cities, a segment underserved by larger lenders.

Their loan portfolio offers both traditional home loans and a variety of “home equity” options, including loans secured against property, commercial real estate loans, and other products.

Source: Repco’s Annual Reports and Q3 FY 24 presentation

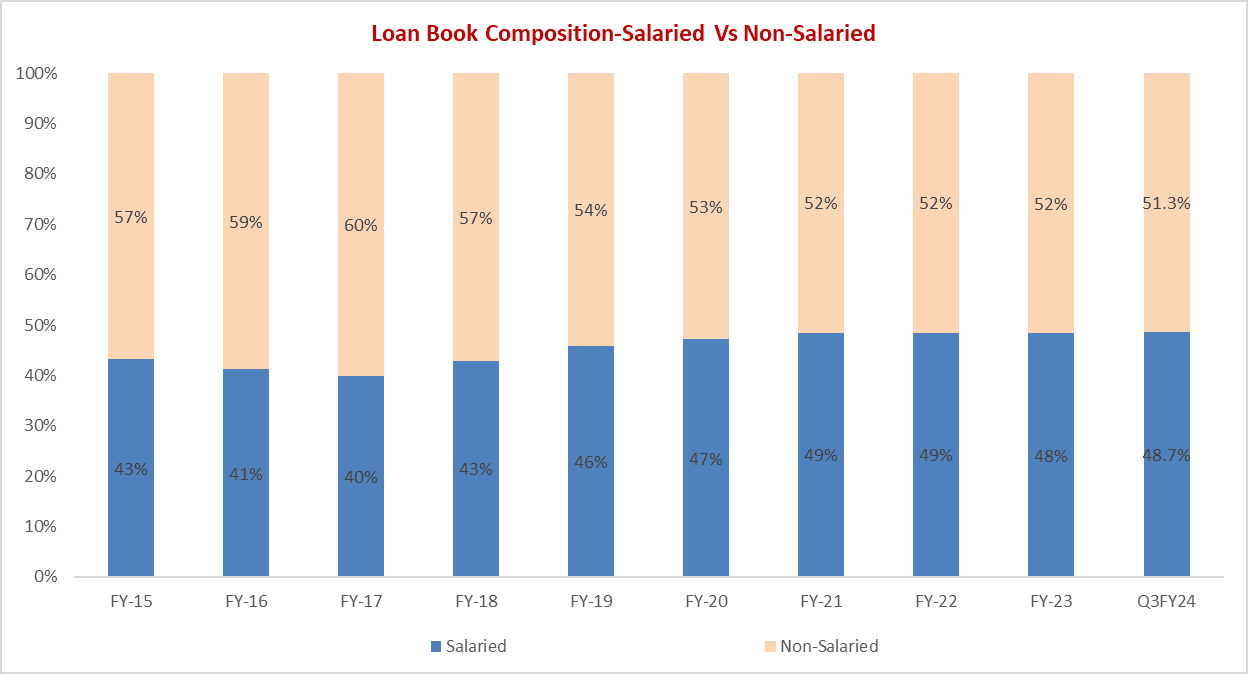

Repco caters to a diverse clientele. Over half (51%) are self-employed non-professionals, while the remaining loans (49%) go to salaried individuals, primarily those considered low-risk borrowers.

Source: Repco’s Annual Reports and Q3 FY 24 presentation

They specialize in providing smaller home loans, with an average loan size of around Rs 12 lakh.

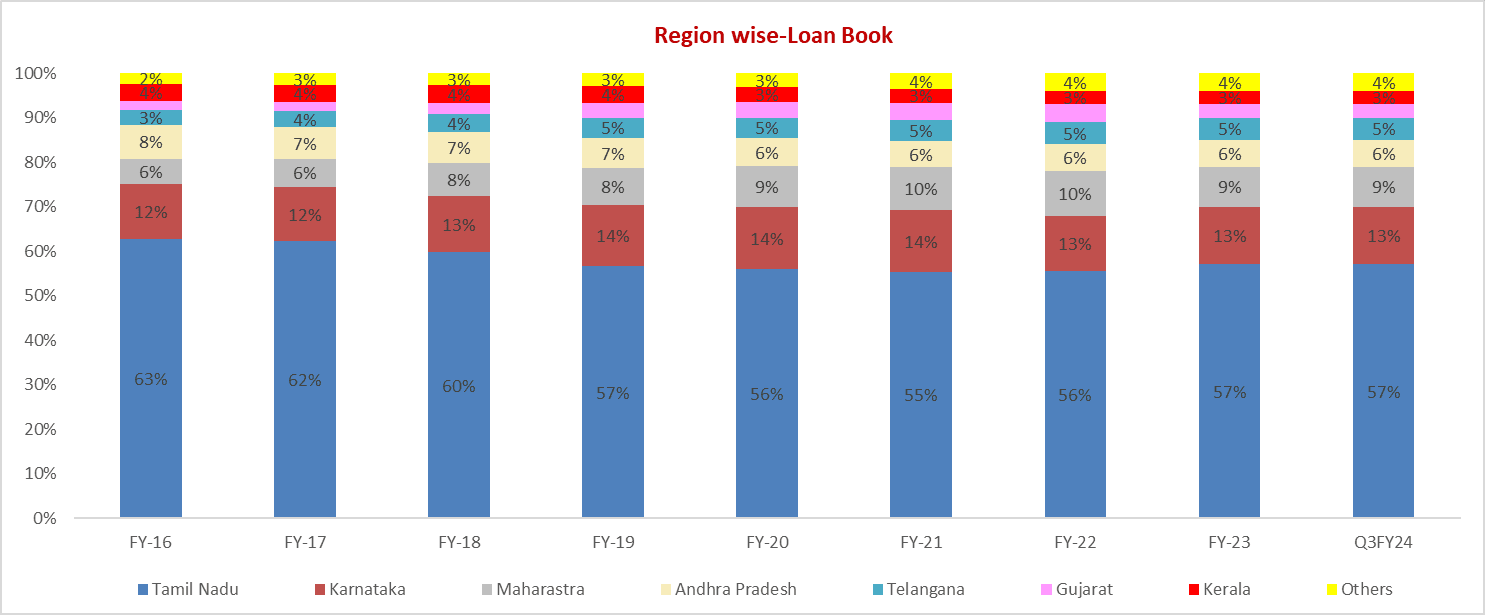

Repco operates through a network of 166 branches and 34 satellite centres spread across 12 states and one Union Territory. Additionally, the company has 2 asset recovery branches.

Notably, a significant portion of their loan portfolio (~80%) is concentrated in South India, with Tamil Nadu (57%) and Karnataka (13%) being their biggest markets.

Source: Repco’s Annual Reports and Q3 FY 24 presentation

Investment Rationale

As mentioned in the sections above, Repco is quoting at < 1 time book value and at around 7 times earnings.

The question is why the valuations are low and if there’s scope for both earnings growth and valuations re-rating.

We believe, the valuations are low because of 2 major factors – slow loan book growth and not so great asset quality.

In the below sections we will look at the reasons for the 2 and if the company is already on the road to recovery.

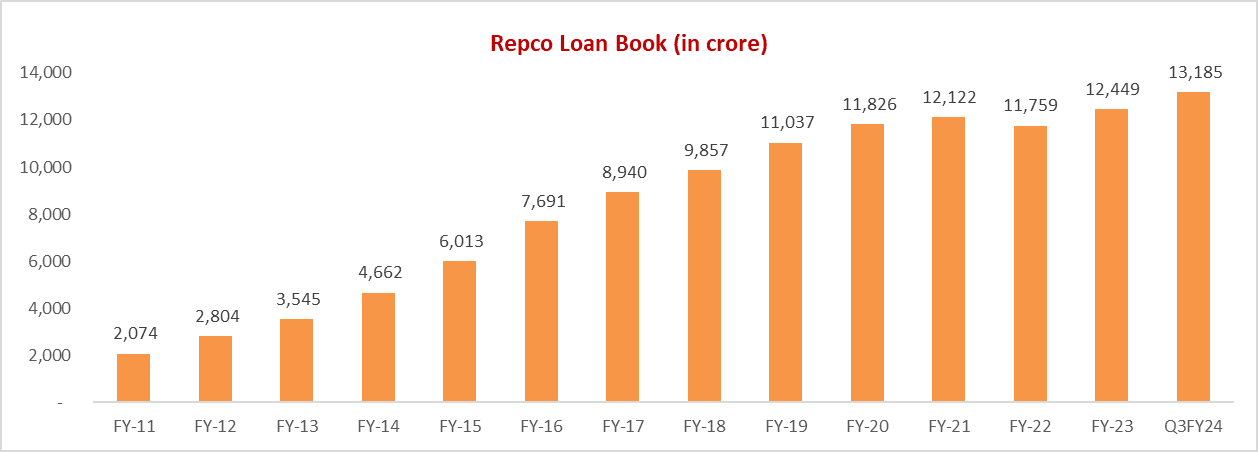

Loan book

Source: Repco’s Annual Reports and Q3 FY 24 presentation

Source: Repco’s Annual Reports and Q3 FY 24 presentation

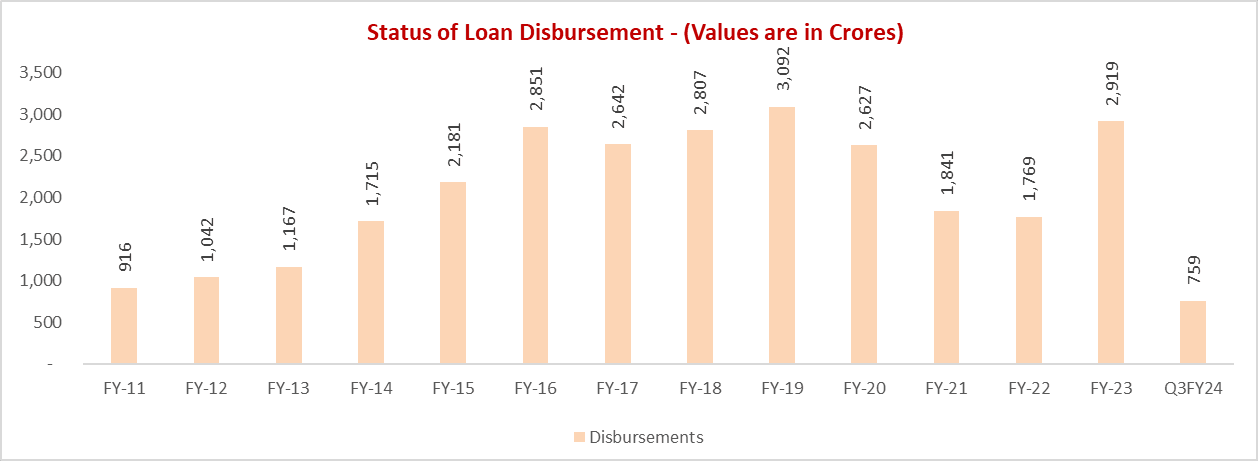

As can be noted from the charts above, there was good credit growth till FY19 (some moderation between FY 17-19); however, between FY 19-FY 23, the loan book growth slowed down to around 3% CAGR with a drastic fall in disbursements till FY 22.

As the company generates more than 50% of loan book from non-salaried segment, the growth got impacted first due to demonetization and GST and later due to Covid-19.

The disbursements improved significantly in FY 23 and have further grown by 7.5% in 9M FY 24 over 9M FY 23.

Under the guidance of new management, the company has taken various steps to accelerate loan book growth.

Earlier, loan generation was largely from walk-in customers and through direct selling agents (DSAs). Since Q4 FY 23, the management has brought in structural changes with verticalization of business and creation of separate verticals for collections and sales.

The company has set up a new sales vertical comprising of ~200 in-house personnel and the same has started contributing ~20% to the current disbursement.

To control BT-outs (balance transfer outs), at the head office level, the company remains in touch with central agencies like CIBIL to get reports about the likelihood of customers moving out. Branches in turn inquire with the customers if they are seeking an interest reduction to prevent such BT-outs.

Source: Repco’s Annual Reports

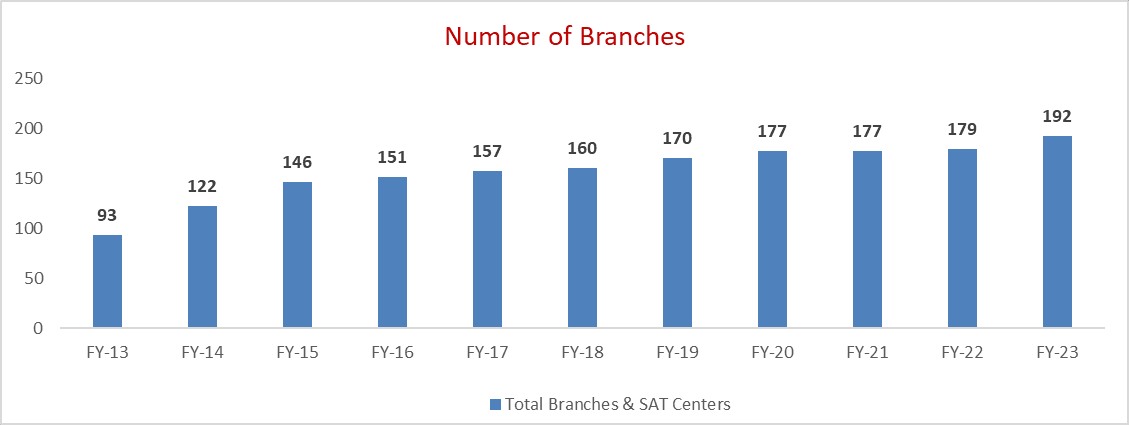

Another aspect the management is working on is branch expansion.

At the end of Dec’23, the company had 166 branches, 34 satellite centres and 2 additional recovery branches. The management is expecting to close FY 24 with 210 centres.

Between FY 19-FY 22, the company opened only 9 new centres; however, the branch addition has gained traction since FY 23. For FY 25-FY 27, the management is targeting to open 40 new branches (50% in Tamil Nadu and 50% in other states) and a loan book of Rs 20,000 crore by Mar’27 in a normal scenario.

Source: Repco’s Q3 FY 24 con-call transcript

Overall, right from simplification of the underwriting process including decentralisation of powers, setting up of 200 personnel sales team, implementation of a new software, controlling BT outs and branch network expansion, the management has taken various steps to accelerate the loan book growth and targeting around 14% CAGR for the next 3 years against only 3% between FY 19-FY 23.

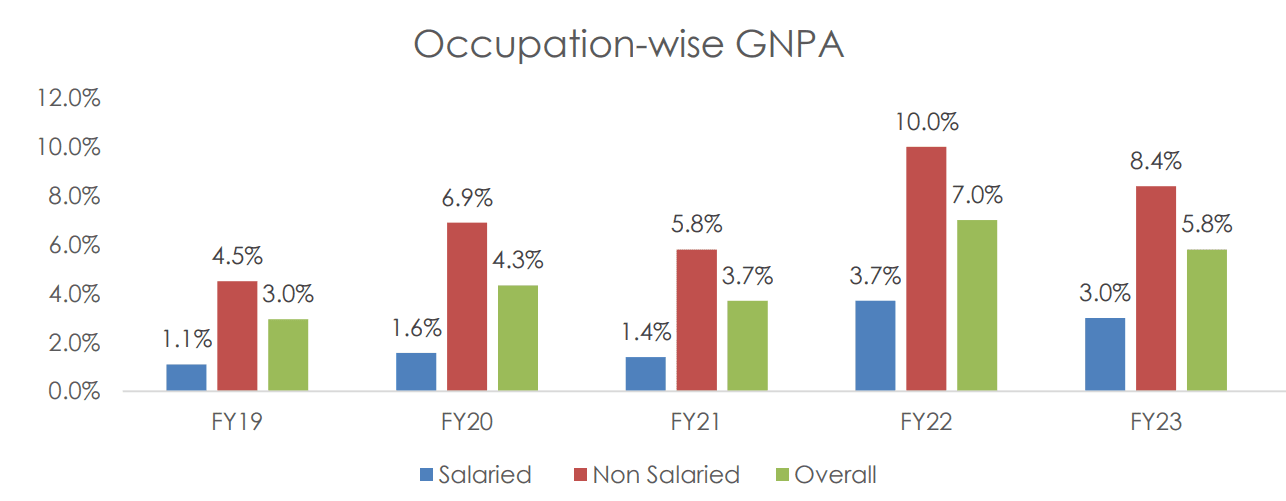

Asset Quality

Source: Repco’s Annual Reports and Q3 FY 24 presentation

Over half (51%) of Repco’s customers are self-employed non-professionals, while the remaining loans (49%) go to salaried individuals, primarily those considered low-risk borrowers.

The asset quality didn’t have any major issues till FY 16; however, starting FY 17, the asset quality started worsening first due to demonetization and GST and later due to Covid-19.

Source: Repco’s Sep’23 Investor Presentation

Demonetization, GST, and later pandemic impacted the cash flows, especially in the non-salaried segment.

As a result, the GNPA reached a peak of 7% in Q3FY22, accompanied by an SMA-2 (Special Mention Accounts) and restructured book exceeding 15% and 5%, respectively.

Under the new management, Repco has created a separate collection vertical from Apr’23, wherein 80 + people primarily focus on collection of current dues as well as Stage-2 assets.

On the NPA side, the company has engaged legal personnel and has sent demand notices to NPA accounts under the SARFAESI Act.

The results have been positive with GNPA reducing to 4.70%, SMA-2 at around 12% and restructured book at around 4.1% in Q3 FY 24. The management expects Stage-2 assets to fall below 10% before FY 24 end.

Besides augmentation of collection efforts, the underwriting standards also seem to have improved as there’s been much lower delinquencies from disbursements made in the last 18-24 months.

Also, despite stress in loan book, as per the management, the ultimate losses have been minimal due to the secured nature of the loans and low LTV (loan to value).

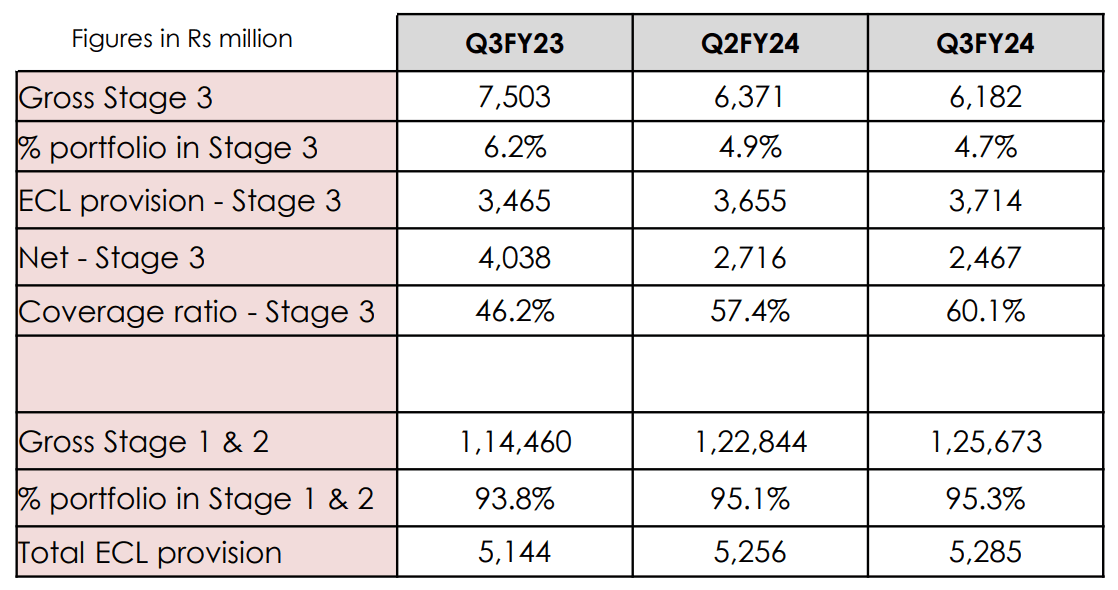

Source: Repco’s Q3 FY 24 presentation

As can be noted above, the GNPA has dropped not just in % terms, but also in absolute terms.

Further, despite the recoveries, the company has been retaining provisions against stage 3 assets resulting in provision coverage ratio – stage 3 increasing to 60.1% in Q3 FY 24 against 46.2% in Q3 FY 23.

Thus, considering the actions being taken, while NPA slippages are likely to be modest, NPA resolutions might be higher. Management has set a target of < 2% GNPA by FY 27.

Source: Repco’s Sep’23 Investor Presentation

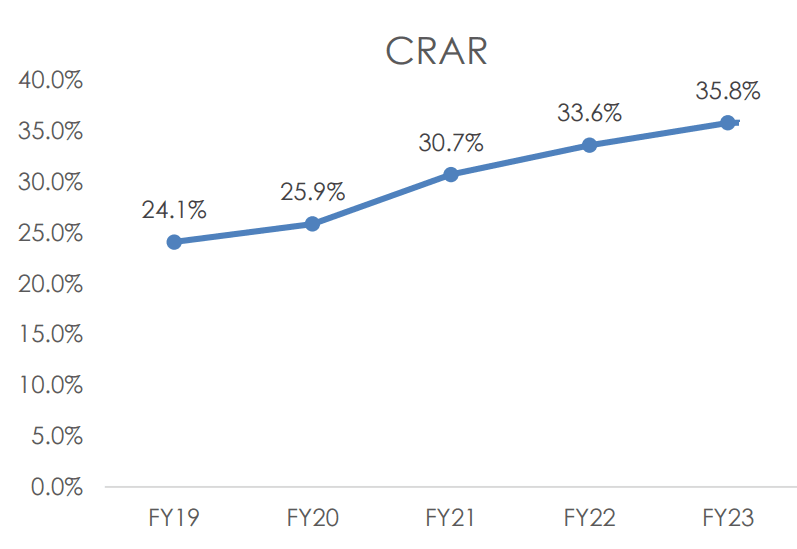

What also gives comfort is Repco’s high capital adequacy of 35% + and relatively low leverage of only around 4x.

Performance

Source: Repco’s Annual Reports

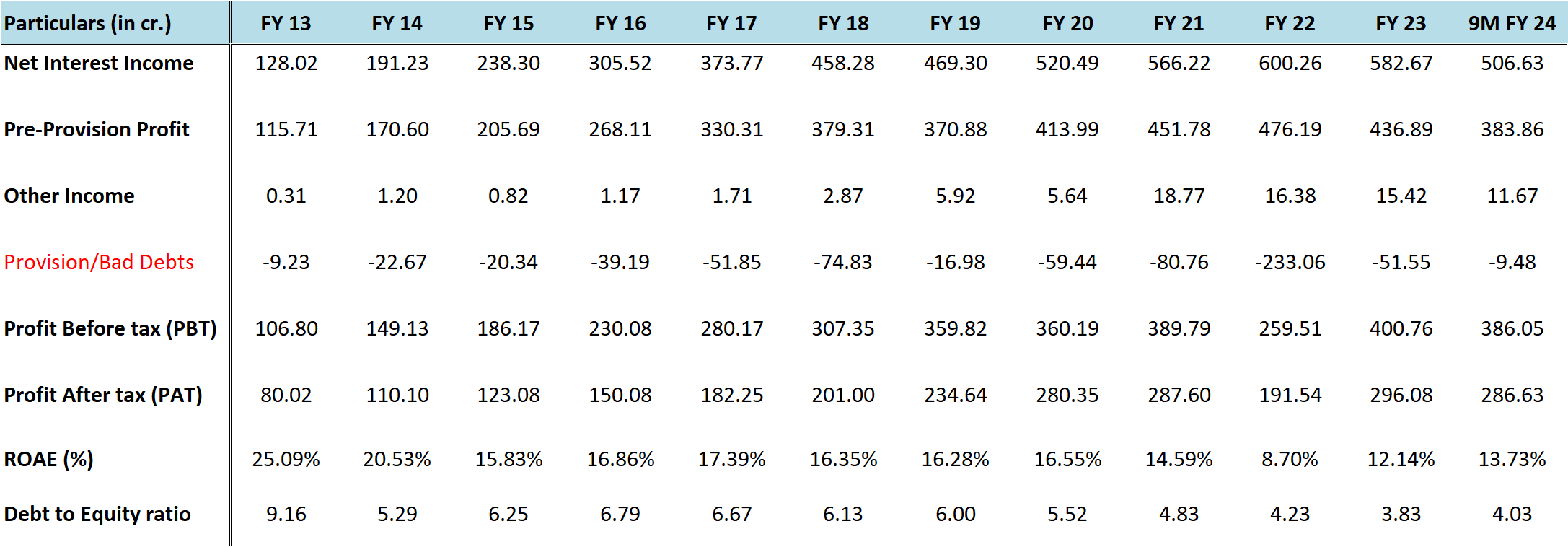

Repco has been delivering healthy performance with strong growth in net interest income till FY 18.

Thereafter the net interest income growth slowed down in tandem with slowdown in loan book growth.

ROAE too moderated due to the above reason and more than adequate capital. As can be noticed, the debt to equity ratio came down from the high of 9.16 in FY 13 to 3.83 in FY 23.

However, as credit growth picks up, ROAE is expected to start improving.

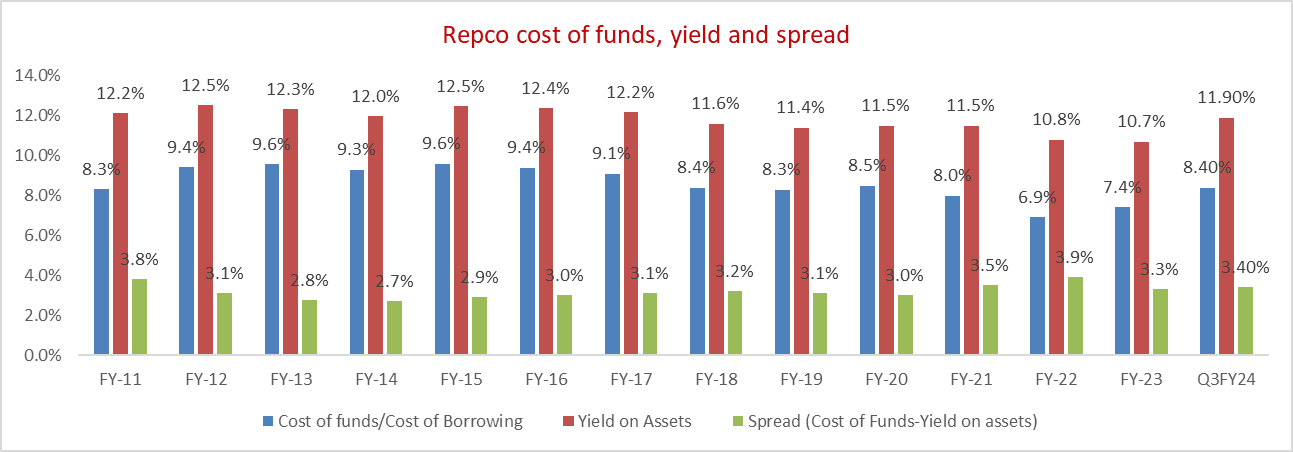

Source: Repco’s Annual Reports and Q3 FY 24 presentation

The company has also done well in terms of maintaining spreads around 3-3.5% consistently; though the same may contract a bit to around 3% as the company is focusing on higher quality customers.

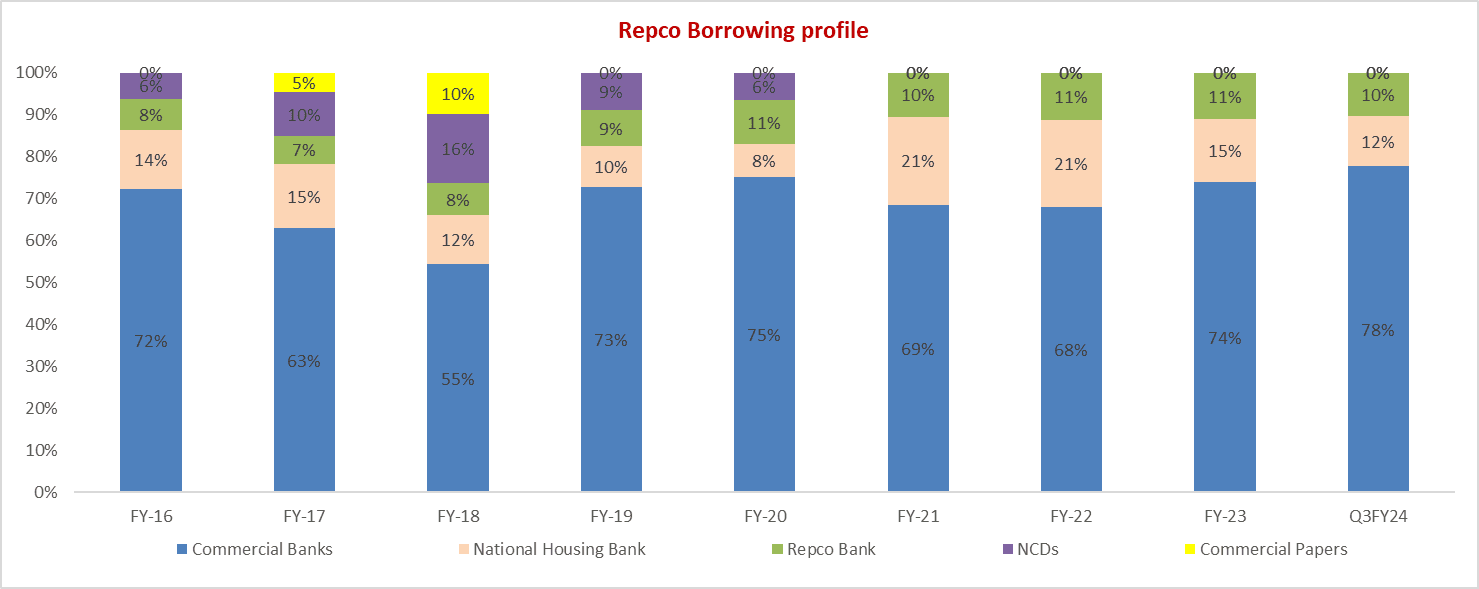

At the same time, company might benefit from lower cost of NHB funding. For the past 1.5-2 years, the company has not been able to avail new borrowing from NHB as it could not meet certain requirements. NHBs contribution in borrowing mix has reduced from 21% in FY 22 to only 12% in Q3 FY 24.

Source: Repco’s Annual Reports and Q3 FY 24 presentation

The company has now become eligible and applied for the same and could help lower the cost of funds and maintain the spreads.

Besides, for the next 2-3 years, apart from regular growth in net interest income on the back of growth in loan book, the company will likely benefit from negligible credit cost or maybe even writeback of excess provisions.

This is because despite the recent recoveries and continued efforts on containing slippages, the company has been retaining provisions against stage 3 assets resulting in provision coverage ratio – stage 3 increasing to 60.1% in Q3 FY 24 against 46.2% in Q3 FY 23.

Valuations

Repco is currently trading at a market cap of Rs 2,500 crore.

The net worth of the company is around Rs 2,750 crore and on TTM basis the company has recorded PAT of Rs 369 crore.

From the above sections we know that the company is moderately leveraged at around 4 times debt to equity which is one of the lowest as per the industry standards.

In the recent past, there have been issues around slow credit growth and asset quality issues; however, as observed in the above sections, the management is tackling both through structural changes and setting up dedicated sales and collections verticals.

Already, there are signs of recovery in credit growth and reduction in non-performing assets and containment of slippages.

By FY 27, the management is targeting loan book of Rs 20,000 crore against current value of around Rs 13,000 crore. This may go up to Rs 25,000 crore in case of favourable external factors. Further, the management is targeting to bring the GNPA down to 2% from 4.7% currently.

During its hey days, the stock used to trade around 4-5 times book value, while in the recent past it went to as low as 0.4-0.5 times book value.

We believe, in the next 3 years, the book value of the company can increase to around Rs 3,800 crore (annual PAT of around Rs 350 crore +). Further, if the management can walk the talk and attain loan book and GNPA targets, there’s high possibility of stock re-rating to 1.5-2 times book value which can be Rs 5,700-7,600 crore market cap against the current market cap of Rs 2,500 crore.

On the downside, assuming lower annual PAT of Rs 200 crore for the next 3 years and book value of Rs 3,500 crore at the end of FY 27, with valuations of 0.5 times book value the market cap can be Rs 1,750 crore.

Thus, the risk-reward ratio looks favourable.

Risks/concerns

Tamil Nadu accounts for 57% of the loan book of the company and southern states around 80% and therefore there’s state and region specific risk.

Non-salaried borrowers account for more than 50% of the loan book of the company. This is a relatively riskier borrower segment in comparison to salaried individuals and therefore asset quality risk remains.

We have factored in growth and asset quality improvement estimates. If the company can’t improve loan book growth while maintaining asset quality, the stock may again de-rate to lower price to book ratio.

Housing finance is a highly competitive market and if the company can’t maintain spreads and NIM while maintaining loan book growth, the profitability will be impacted.

Disclosure: I don’t have any investment in Repco Home finance and have not traded in the stock in the last 30 days.

Best Regards,

Ekansh Mittal

Research Analyst

http://www.katalystwealth.com/

Ph.: +91-727-5050062, Mob: +91-9818866676

Email: [email protected]

Rating Interpretation

Positive – Expected return of ~15% + on annualized basis in medium to long term for investment recommendations and in short term for Special situations

Neutral – Expected Absolute return in the range of +/- 15%

Negative – Expected Absolute return of over -15%

Coverage closure – No further update on the stock

% weightage – This is based on our 20-25 stocks investment philosophy. Members are free to make allocation of their choice (if you invest) or consult their Investment Advisor for the same

Short term – Less than 1 year

Medium term – Greater than 1 year and less than 3 years

Long term – Greater than 3 years

Research Analyst Details

Name: Ekansh Mittal Email Id: [email protected] Ph: +91 727 5050062

Analyst ownership of the stock: No

Details of Associates: Not Applicable

Analyst Certification: The Analyst certify (ies) that the views expressed herein accurately reflect his (their) personal view(s) about the subject security (ies) and issuer(s) and that no part of his (their) compensation was, is or will be directly or indirectly related to the specific recommendation(s) or views contained in this research report.

Disclaimer: www.katalystwealth.com (here in referred to as Katalyst Wealth) is the domain owned by Ekansh Mittal. Mr. Ekansh Mittal is the sole proprietor of Mittal Consulting and offers independent equity research services to retail clients on subscription basis. SEBI (Research Analyst) Regulations 2014, Registration No. INH100001690

Address – 7, Panch Ratan, 7/128, Swaroop Nagar, Kanpur – 208002, Contact No. – +91-7275050062

Compliance Officer – Mr. Ekansh Mittal, +91-9818866676, [email protected]

Grievance Redressal – Mittal Consulting, [email protected], +91-9818866676, +91-7275050062

“Registration granted by SEBI and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors”.

Performance numbers do not include the impact of transaction fee and other related costs. Past performance does not guarantee future returns.

“Investment in securities market are subject to market risks. Read all the related documents carefully before investing.”

The views expressed are based solely on information available publicly and believed to be true. Investors are advised to independently evaluate the market conditions/risks involved before making any investment decision.

A graph of daily closing prices of securities is available at www.bseindia.com (Choose a company from the list on the browser and select the “three years” period in the price chart.

This report is for the personal information of the authorized recipient and does not construe to be any investment, legal or taxation advice to you. Ekansh Mittal/Mittal Consulting/Katalyst Wealth is not soliciting any action based upon it. This report is not for public distribution and has been furnished to you solely for your information and should not be reproduced or redistributed to any other person in any form. This document is provided for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision. Ekansh Mittal or any of its affiliates or employees shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. Neither Ekansh Mittal, nor its employees, agents nor representatives shall be liable for any damages whether direct or indirect, incidental, special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information. Ekansh Mittal/Mittal Consulting or any of its affiliates or employees do not provide, at any time, any express or implied warranty of any kind, regarding any matter pertaining to this report, including without limitation the implied warranties of merchantability, fitness for a particular purpose, and non-infringement.

The recipients of this report should rely on their own investigations. Ekansh Mittal/Mittal Consulting and/or its affiliates and/or employees may have interests/ positions, financial or otherwise in the securities mentioned in this report. Mittal Consulting has incorporated adequate disclosures in this document. This should, however, not be treated as endorsement of the views expressed in the report.

We submit that no material disciplinary action has been taken on Ekansh Mittal by any regulatory authority impacting Equity Research Analysis.

Disclosure (SEBI RA Regulations)

Whether the research analyst or research entity or his associate or his relative has any financial interest in the subject company/companies and the nature of such financial interest – No

Whether the research analyst or research entity or his associates or his relatives have actual/beneficial ownership of 1% or more securities of the subject company (at the end of the month immediately preceding the date of publication of the research report or date of the public appearance) – No

Whether the research analyst or research entity or his associate or his relative has any other material conflict of interest at the time of publication of the research report or at the time of public appearance – No

Whether it or its associates have received any compensation from the subject company in the past twelve months – No

Whether it or its associates have managed or co-managed public offering of securities for the subject company in the past 12 months – No

Whether it or its associates have received any compensation for investment banking or merchant banking or brokerage services from the subject company in the past 12 months – No

Whether it or its associates have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company in the past 12 months – No

Whether the subject company is or was a client during twelve months preceding the date of distribution of the research report and the types of services provided – No

Whether the research analyst has served as an officer, director, or employee of the subject company – No

Whether the research analyst or research entity has been engaged in market making activity for the subject company – No