Dear Members,

We have released 22nd Nov’22: Chaman Lal Setia Exports Ltd (NSE Code – CLSEL) – Alpha/Alpha Plus stock for Nov’22. For details and other updates, please log into the website at the following link – http://katalystwealth.com/index.php/my-account/

Note: For any queries, mail us at [email protected]

Date: 22nd Nov’22

CMP – 112.70 (BSE); 112.80 (NSE) Face Value – 2.00

Rating – Positive – 4% weightage (this is not an investment advice, refer rating interpretation)

Introduction

We have recommended Chaman Lal Setia (CLSE) twice in the past.

In Nov’16 we recommended CLSE at around 60 odd levels and closed it in Dec’17 at around 150 odd levels.

In Sep’19, we recommended CLSE around 46 odd levels and closed it in May’21 around 133 odd levels.

At the time of closure, despite liking CLSEs focus on efficient working capital management and reasonable valuations, we were concerned that earnings may have peaked out for the near future.

In FY 22, the company did report contraction in EBITDA margins and 20% drop in PAT. However, since then, on the back of strong volume growth and higher realizations, the TTM PAT is back to FY 21 levels and the valuations are even lower as the stock is down 15% from May’21 levels.

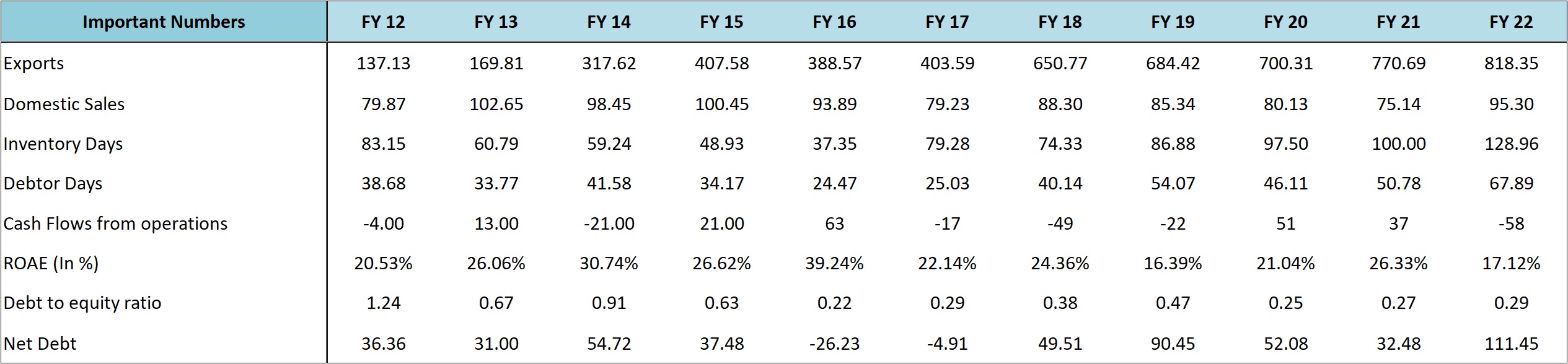

Regarding growth, despite the overall basmati exports from India remaining flattish from FY 15 to FY 22, the company’s share in the exports has doubled from 1.5% in FY 15 to 3.1% in FY 22. The company has been continuously gaining market share in basmati exports as its share was only 0.9% in FY 12.

We believe, the stock offers a decent opportunity around current levels as the valuations look reasonable at around 7.25 times TTM earnings and 1.29 times book value.

Over the last 5 years, (excluding covid lows) the Price to book value ratio of the company has gyrated between 0.9 to 3.6.

Basmati rice industry has seen collapse of several listed players and all of them were highly leveraged and had working capital issues. What we like the most about CLSE is its differentiated approach to business and focus on maintaining an asset light balance sheet.

Business details

Promoted by Chaman Lal Setia, Vijay Setia and Rajeev Setia, Chaman Lal Setia Exports Limited (CLSE) was incorporated as a partnership firm in 1975, under the name Chaman Lal & Sons.

In 1995, it went public under its present name to finance the expansion and modernisation of the units.

- CLSE is engaged in the business of milling, processing and trading of basmati rice

- The company has a paddy unit in Karnal (Haryana) and Amritsar (Punjab). In Karnal it has a milling capacity of 12 tonne per hour and sorting capacity of 40 tonne per hour

- The company also has rice grading and sorting facilities in Amritsar (Punjab) and Kandla (Gujarat)

- CLSE derives 90-95% revenue primarily from one segment i.e., sale of basmati rice. Besides purchasing paddy and processing at its own unit, the company is also engaged in procurement and sale of semi-processed rice

- Product range covers raw, steamed and parboiled rice. The company also has innovative products in its portfolio i.e., diabetic’s basmati rice, pesticide-free basmati rice, etc

- Export of Basmati rice accounts for 85-90% of the turnover of the company

- In exports, the company primarily caters to the private label business while the domestic sales are under its own brands: Mithas, Begum and Maharani

- Overall, the company generates 25-30% of the sales from its own brands

- The company has a loyal client base of more than 400 buyers spread across more than 80 countries such as USA, UAE, Mauritius, Saudi Arabia, Malaysia, Kuwait, New Zealand, Australia and Singapore, among others

- CLSE has one of the most diversified geographical and customer profile as demonstrated by penetration having increased to over 80 countries compared to 60 countries 4 years back

- As per the management, no single country accounts for a very large share of exports as the company has been exploring markets outside the traditional Middle Eastern countries

- CLSE doesn’t export to Iran directly even though Iran along with Saudi Arabia accounts for 40-50% of basmati rice exports from India

Source: https://www.clsel.in

CLSE follows a slightly differentiated business model for basmati rice:

- It acts more like a trader and focused largely on exports and private label business

- The management believes in dealing in smaller consignments, multiple buyers across multiple countries

- The company has a small presence in domestic markets

- The management doesn’t believe much in the idea of ageing of rice and therefore stocks much lower inventory than its peers

Basmati rice industry – Overview

After wheat and maize, rice is the world’s third principal staple food and is cultivated in more than 113 countries. Over 90% of the global rice output and consumption is centred in Asia, wherein the world’s largest rice producers, China and India, are also the world’s largest rice consumers.

There are two varieties of rice: Indica and Japonica. Basmati is an Indica variety.

Indica rice is long-grain rice and is usually grown in hot climate. This rice is fluffy and doesn’t stick together on cooking. Japonica is a short-grain variety of rice (fat and round grain) which is mainly characterized by its unique stickiness and remains moist, which helps it to be eaten with chopsticks.

Rice can be consumed in three forms i.e., white rice, brown rice and parboiled rice. White rice is the polished rice because both the outer layers i.e., husk and bran are removed. In brown rice only the husk is removed while the bran layer remains.

Parboiled rice undergoes an additional process of boiling and steaming to capture the nutritive value of bran in the rice. Parboiled rice has good demand in Middle East.

Basmati rice – Basmati rice accounts for ~2-3% in terms of volumes of the global rice industry. India accounts for over 70% of the world’s basmati rice production and the rest is accounted for by Pakistan.

Basmati is unique to the region. It can be grown where precise climatic conditions; soil quality and temperature exist and this only occurs in the Indo-Gangetic area of the Himalayas. It is also legally protected as a trade name. “Basmati” is protected under “The Geographical Indications of Goods (Registration & Protection) Act, 1999” of India, which prevents any rice grown outside of the Indo Gangetic area from being called Basmati.

Basmati rice constitutes a small portion (<10%) of the total rice produced in India; though it accounts for ~20% in volume terms and ~60% in value terms of India’s total rice exports.

PUSA 1121 (PB1121) – There have been various varieties of Basmati notified under the Seed Act, 1966. PUSA 1121, which was developed in FY04, was in FY11 notified by the Government of India as a Basmati variety.

PUSA 1121 has significantly altered the supply dynamics of the industry. Its share in total Basmati paddy cultivation is now more than 65% and has cannibalized other Basmati varieties and expanded the segment. PUSA 1121 has significant advantages over traditional varieties of Basmati.

The other approved Indian varieties include Dehradun, P3 Punjab, 386 Haryana, Kasturi (Baran, Rajasthan), Basmati 198, Basmati 217, Basmati 370, Bihar, Kasturi, Mahi Suganda, Pusa 1121, Pusa 1509 and PUSA 1718.

PUSA 1847, PUSA 1885 and PUSA 1886 – Harvested for the first time this season — the 3 varieties have been developed by Indian Agricultural Research Institute.

The 1847, 1885 and 1886 are improved versions of the PUSA 1509, 1121 and 6, respectively, which accounted for 90% of the Basmati rice exports from India.

They are disease-free, use half the water, cost less to grow, give higher yield and fetch higher prices and are being considered revolutionary.

The need for developing these varieties arose in order to curb bacterial blight and blast diseases which affect the yield and grain significantly. Traditionally, these diseases were treated through chemicals like streptocycline and tricyclazole.

The 3 varieties can also help increase exports to EU and other countries as there’s greater demand for pesticide free basmati.

PUSA varieties creating level playing field – Earlier, certain rice processors were known for their ability to select finer quality paddy out of the traditional Basmati varieties, but that advantage is no longer relevant as most Basmati being grown is PUSA 1121. Whatever limited product differentiation existed are slowly being eroded due to increasing homogeneity of Basmati.

Ageing of Basmati – While companies like KRBL, L T Foods have created brands like India Gate, Daawat, etc on the premise of ageing of rice and sell their products at some premium to other brands; the management of CLSE doesn’t believe much in the significance of ageing.

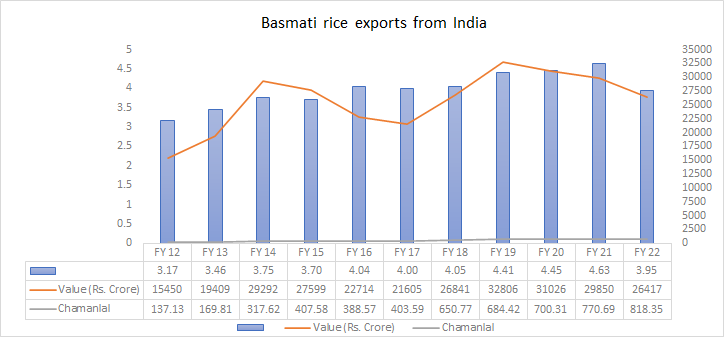

Basmati Exports – India’s Basmati rice exports increased at an astounding CAGR of 26% from Rs 2,824 crore in 2004-05 to Rs 27,598 crore in 2014-15.

Source: APEDA Agriexchange

Since FY 15, the exports have been flattish with last 3 years reporting sequential decline in value terms, even though the basmati export volumes have been inching up year on year.

What is interesting to note is that despite the flattish basmati rice exports (in value terms) over the last few years, CLSE has been growing and gaining market share.

Source: CLSE Annual Reports, APEDA Agriexchange

For H1 FY 23, the basmati exports have increased by 37.34% on YOY basis to Rs 17,987 crore. This is on the back of 11% increase in volume terms, 24% increase in realizations in USD terms and the remaining through exchange gain.

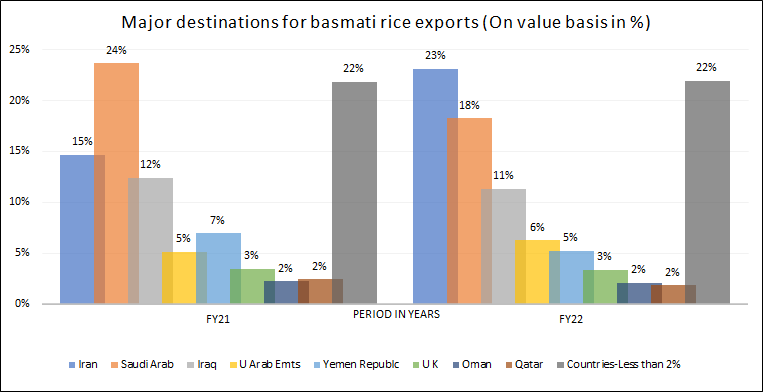

While basmati rice is consumed across the globe, West Asian countries account for ~60-70% of Indian basmati rice exports. Within West Asia, Iran and Saudi Arabia are the two largest buyers, together accounting for over 40% of basmati rice exports from India.

Source: APEDA Agriexchange

Promoters/Management

Chaman Lal Setia Exports is an owner operated business with Mr. Vijay Setia and Mr. Rajeev Setia at the helm of the affairs of the company.

Mr Vijay Setia is an Ex-President of All India Rice Exporters Association. Regd. (AIREA), Delhi. He has also worked with M/s. Gerson Lehrman Group as a consultant in the field of Food Technology for having in-depth knowledge of the subject.

The company has also seen induction of 3rd generation promoters with Mr. Ankit Setia and Mr. Sankesh Setia taking keen interest in the operations of the company.

As per Mr. Rajeev Setia, both Ankit and Sankesh have been exploring the export opportunities in a big way and have been adding customers in new countries.

Overall, the promoters have run the company well and much more efficiently than some of the larger listed peers.

The promoters own more than 70% stake in CLSE and therefore their interests are directly aligned with those of shareholders. They have also extended long term deposits worth Rs 55-56 crore to the company and on the same they charge interest of 9% p.a.

Source: CLSE Annual Reports

What is also interesting to note is that CLSE has been consistently paying dividends since 1996 (barring 2002); however, we believe the quantum of dividend pay-out can be increased.

Looking at the strong balance sheet of CLSE, we also believe that there’s no need for long term deposits from the promoter and a better way to reward both the promoters and the shareholders would be through higher dividend pay-out.

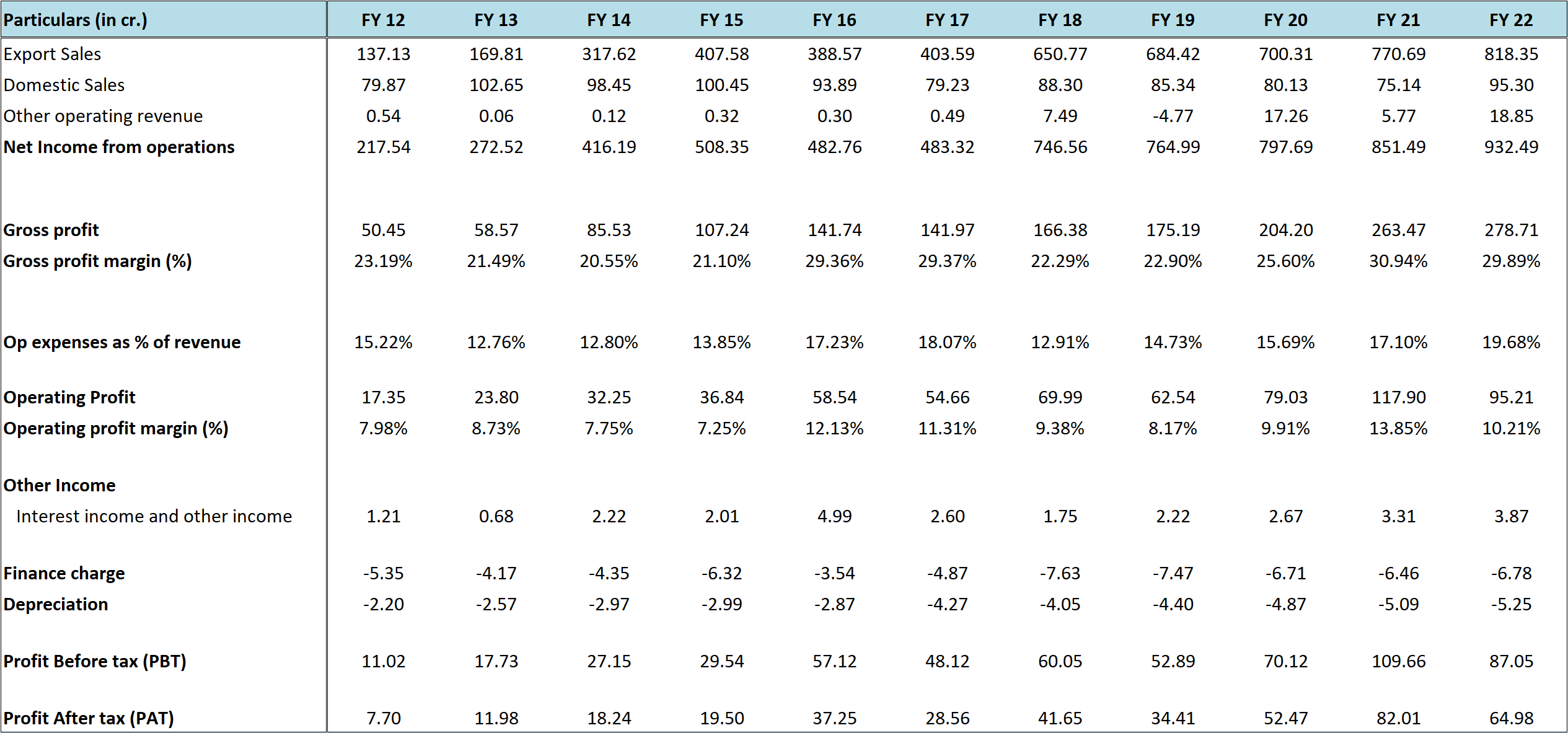

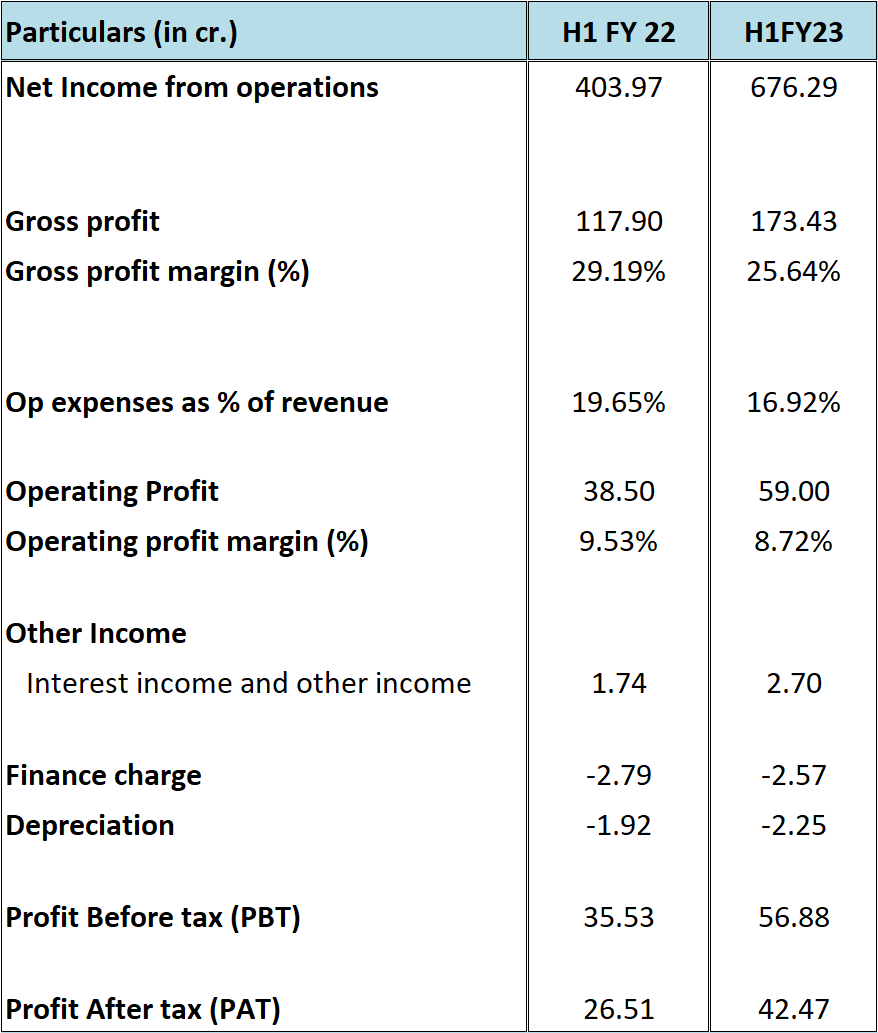

Performance Snapshot

Source: CLSE Annual Reports

Processing and trading of basmati rice has seen several companies go bankrupt on failing to efficiently manage working capital and leverage on the balance sheet. Within the listed space as well, companies like Usher Agro, REI Agro, Kohinoor Foods, etc have either gone bankrupt or are on the verge of the same.

Companies like KRBL, L T Foods have created brands like India Gate, Daawat, etc. on the premise of ageing of rice and command premium pricing for their export and domestic sales; however, at the same time they carry higher amounts of inventory on their balance sheet.

Source: CLSE, KRBL, LT Foods Annual Reports

Thus, CLSEs focus has primarily been on trading of basmati rice and as a result it hasn’t expanded capacity, nor does it carry too much inventory on its books. In fact, the core focus of CLSE is marketing and the management has been trying to expand in both existing markets and looking for new geographies.

The only space where CLSE has expanded capacity is packing facility. As per the management, they have all kinds of packing available: half a kg, 1 kg pouch, 2kg jars, 5kg bags, conventional bags, one-time bags, etc as buyers in different countries have different requirements.

Margins – Over the last few years the gross margins of CLSE have hovered in the range of 22-30%.

Similarly, the EBITDA margins have also hovered in the range of 8-13%.

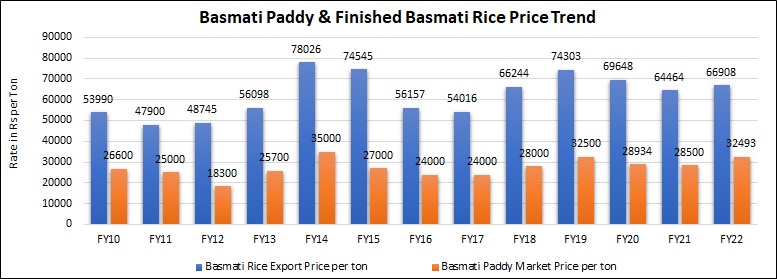

Below, we have shared the Basmati paddy prices (mandi) and export realizations per ton.

Source: APEDA Agriexchange

Taking into account the reported performance of the company for the last 10 years and the paddy and the export prices, our observation is that when paddy and rice prices go down, the gross margins of the company expand, case in point: FY 12, FY 16, FY 17, FY 20 and FY 21.

For H1 FY 23, as the basmati paddy and rice prices have increased, the gross margins of the company have contracted to 25.64% and EBITDA margins to 8.72%; however, the sales have increased by 67%.

Source: CLSE Sep’22 Results update

Thus, in case there’s correction in paddy and rice prices, even though the sales turnover may contract, the company might still be able to maintain or improve the profitability on the back of improvement in margins.

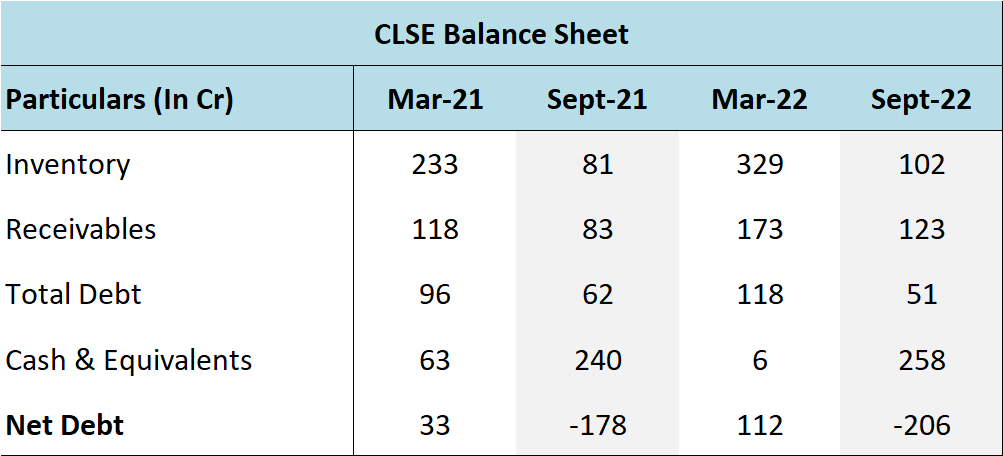

Seasonality in Balance sheet – Owing to the seasonality of rice harvest (October to December), the procurement of raw material goes up in the 2nd Half of the financial year and as a result the inventory and the debt is much higher at the end of the financial year than during the whole financial year.

Source: CLSEs Annual Reports, BSE filings

As can be seen from the above illustration, at the end of H1 FY 22 (Sep’21), the company was cash rich with ~ Rs 178 crore of surplus cash.

Similarly, as per the latest Sep’22 results filing, CLSE had surplus cash and equivalents of Rs 206 crore.

Source: CLSE Annual Reports

As can be seen from the above illustration, in an industry where the mortality rate is high, CLSE is not only surviving, it has been performing reasonably well by adopting a differentiated approach of trading and not necessarily trying to establish a brand based on the ageing of rice.

As a result, the company has been consistently doing well on various metrics like working capital management, leverage and return on equity.

Valuations

From the above sections we know the following:

- Basmati rice can be grown only in India and Pakistan with India accounting for 70% market share

- Basmati rice industry has high mortality rate with several listed companies having gone bankrupt

- The primary reason for bankruptcy seems to be fixation with ageing of rice and maintaining high level of inventory and thereby debt

- CLSE considers Basmati rice a commodity and follows a differentiated approach of trading in the same than focusing excessively on manufacturing and ageing

- The company is largely focused on exports and has been actively seeking new geographies. The company doesn’t export to Iran, even though Iran accounts for the largest share of Basmati rice exports from India

- CLSE has 3% share in Basmati rice exports from India and could probably capture higher market share with the collapse of other companies

- The promoters of the company have long standing experience with 3rd generation joining the business

- Their interests are directly aligned on account of more than 70% stake in the company

- Despite the twists and turns in Basmati rice exports from India and substantial changes in paddy and rice prices, the company has been quite consistent in terms of maintaining its sales and profitability

- CLSE has consistently done well on metrics like working capital management, leverage, return ratios, etc

- Last, but not the least, CLSE has been paying dividends since 1996 (barring only 2002)

- At around current price of 110-115, the market cap of CLSE is around 590 crores. The net debt at the end of Mar’22 was around 112 crores; however, looking at the finance cost the average debt for the year should be around 70 crores

The stock is currently trading around 7.25 times trailing twelve months earnings (8.9 times 3 years average PAT) and the Price to Book value is 1.29. Over the last 5 years, (excluding covid lows) the Price to book value ratio of the company has gyrated between 0.9 to 3.6.

If there’s major drop in export realizations, there could also be contraction in margins in the short term (inventory loss); however, as we have seen in the past, the company has generally done well even during periods of lower realizations and exports and the margins and the balance sheet have improved during such times.

Risks/concerns

CLSE derives 85-90% of its sales from exports. Wide fluctuations in currency can impact the profitability of the company negatively.

The Middle East is the biggest export market for Indian basmati rice and accounts for over 60-70% of its exports. Hence, any political turmoil in this region may adversely impact India’s exports.

European Union has implemented stricter norms on use of pesticides for import of various crop varieties and the same has impacted sales to the region.

While CLSE doesn’t sell to Iran, it could still face heightened competition from other players as they too may start exploring countries outside of Iran.

While CLSE doesn’t carry very high inventory; however, significant drop in prices of Basmati rice can impact the profitability in the short term.

Disclosure: I have personal investment in Chaman Lal Setia Exports and have not traded in the stock in the last 30 days.

Best Regards,

Ekansh Mittal

Research Analyst

http://www.katalystwealth.com/

Ph.: +91-727-5050062, Mob: +91-9818866676

Email: [email protected]

Rating Interpretation

Positive – Expected return of ~15% + on annualized basis in medium to long term for investment recommendations and in short term for Special situations

Neutral – Expected Absolute return in the range of +/- 15%

Negative – Expected Absolute return of over -15%

Coverage closure – No further update on the stock

% weightage – allocation in the subject stock with respect to equity investments

Short term – Less than 1 year

Medium term – Greater than 1 year and less than 3 years

Long term – Greater than 3 years

Research Analyst Details

Name: Ekansh Mittal Email Id: [email protected] Ph: +91 727 5050062

Analyst ownership of the stock: Yes

Details of Associates: Not Applicable

Analyst Certification: The Analyst certify (ies) that the views expressed herein accurately reflect his (their) personal view(s) about the subject security (ies) and issuer(s) and that no part of his (their) compensation was, is or will be directly or indirectly related to the specific recommendation(s) or views contained in this research report.

Disclaimer: www.katalystwealth.com (here in referred to as Katalyst Wealth) is the domain owned by Ekansh Mittal. Mr. Ekansh Mittal is the sole proprietor of Mittal Consulting and offers independent equity research services to retail clients on subscription basis. SEBI (Research Analyst) Regulations 2014, Registration No. INH100001690

The views expressed are based solely on information available publicly and believed to be true. Investors are advised to independently evaluate the market conditions/risks involved before making any investment decision.

A graph of daily closing prices of securities is available at www.bseindia.com (Choose a company from the list on the browser and select the “three years” period in the price chart.

This report is for the personal information of the authorized recipient and does not construe to be any investment, legal or taxation advice to you. Ekansh Mittal/Mittal Consulting/Katalyst Wealth is not soliciting any action based upon it. This report is not for public distribution and has been furnished to you solely for your information and should not be reproduced or redistributed to any other person in any form. This document is provided for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision. Ekansh Mittal or any of its affiliates or employees shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. Neither Ekansh Mittal, nor its employees, agents nor representatives shall be liable for any damages whether direct or indirect, incidental, special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information. Ekansh Mittal/Mittal Consulting or any of its affiliates or employees do not provide, at any time, any express or implied warranty of any kind, regarding any matter pertaining to this report, including without limitation the implied warranties of merchantability, fitness for a particular purpose, and non-infringement.

The recipients of this report should rely on their own investigations. Ekansh Mittal/Mittal Consulting and/or its affiliates and/or employees may have interests/ positions, financial or otherwise in the securities mentioned in this report. Mittal Consulting has incorporated adequate disclosures in this document. This should, however, not be treated as endorsement of the views expressed in the report.

We submit that no material disciplinary action has been taken on Ekansh Mittal by any regulatory authority impacting Equity Research Analysis.

Disclosure (SEBI RA Regulations)

Whether the research analyst or research entity or his associate or his relative has any financial interest in the subject company/companies and the nature of such financial interest – Yes

Whether the research analyst or research entity or his associates or his relatives have actual/beneficial ownership of 1% or more securities of the subject company (at the end of the month immediately preceding the date of publication of the research report or date of the public appearance) – No

Whether the research analyst or research entity or his associate or his relative has any other material conflict of interest at the time of publication of the research report or at the time of public appearance – No

Whether it or its associates have received any compensation from the subject company in the past twelve months – No

Whether it or its associates have managed or co-managed public offering of securities for the subject company in the past 12 months – No

Whether it or its associates have received any compensation for investment banking or merchant banking or brokerage services from the subject company in the past 12 months – No

Whether it or its associates have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company in the past 12 months – No

Whether the subject company is or was a client during twelve months preceding the date of distribution of the research report and the types of services provided – No

Whether the research analyst has served as an officer, director or employee of the subject company – No

Whether the research analyst or research entity has been engaged in market making activity for the subject company – No