Hello Sir,

Hope you are doing well.

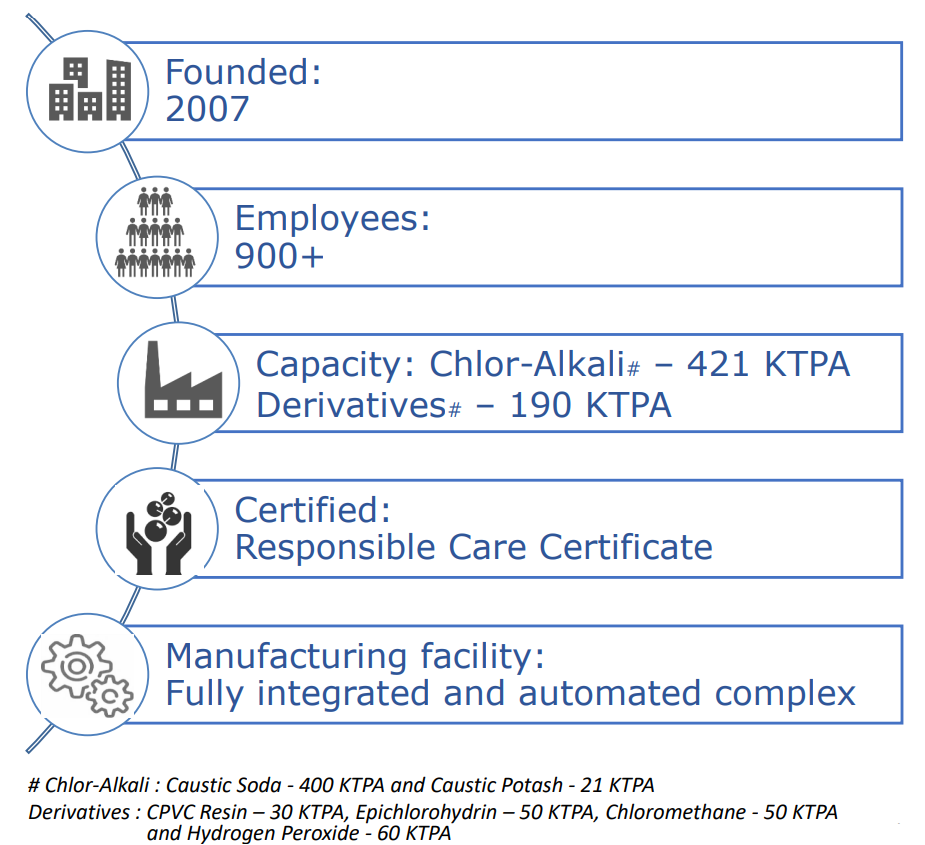

Recently, I was scanning through some stocks and came across Epigral Ltd which is one of the largest Chlor-Alkali and its derivatives manufacturer in India.

In case you have never heard of Epigral before, that’s because, earlier its name was Meghmani Finechem.

Source: Q4 FY 23 presentation

The company is transitioning from Chlor Alkali to its derivatives and specialty chemicals segment.

What’s interesting is that the company’s operating margins are very high at around 30% and the management targets 25% ROCE when setting up any new project.

Below, we have shared interesting insights from the Q1 FY 24 con-call of Epigral to understand the current situation and their expansion plans. Hope you find the details useful for your own investments or to add the stock to your watch list.

We have released 2 new stock recommendations in the last few days:

- 1 Special situation opportunity – We believe, change in ownership along with already strong profitability and growth can result in re-rating of the company to higher valuations. Further, the stock is consolidating in a tight range and the open offer price caps the downside – Details @ (opens in new tab)click HERE

- 1 medium-long term investment recommendation – It’s a sub 3,000 crore market cap company wherein we are expecting company might double its profit in the next 3-4 years. Details @ (opens in new tab)click HERE

You can access the above recommendations and more by subscribing (opens in new tab)HERE

Epigral – Insights from Q1 FY 24 con-call of the company

– General

- Board of Directors had proposed renaming the Company to Epigral

- FY 24 started with a quarter that witnessed events like global level slowdown and destocking impacting the chemical industry both at demand level and also at realization level

- Q1 FY 24 revenue was down by 15% YOY. This is mainly on account of realization which was down by around 26%. However, the volume has gone up by 11% with commissioning of the new capacity of CPVC and epichlorohydrin

- This volume growth is in line with our expansion plan resulting in volume coming from CPVC, epichlorohydrin, and hydrogen peroxide

- This resulted in revenue contribution from derivatives and specialty chemicals at 38% compared to 21% from similar period last year

- The 38% as you would know consists of the chloromethanes, hydrogen peroxide, ECH, and CPVC

- The raw material prices, which have softened but not as substantial as decrease in our realization, thus impacting the profitability margin of the Company

- From July onwards, we are seeing a couple of raw materials started going upward. So, I don’t think any inventory loss will be there from quarter 2 onwards in majority of the companies

– Caustic soda

- We have run a plant of caustic soda on a capacity utilization of around 70% to 75%

- In terms of realizations, if we look about, then the caustic soda realizations have dropped around 40% compared to what it was in the quarter last year

- Caustic soda realization, the ECU that we see is around Rs 30,500

- The last quarter I would say it is exceptional because the energy price has not fallen because of the high cost of inventory also and the caustic price has fallen much faster

- But we are expecting almost 25% EBITDA from the caustic soda business

– Epichlorohydrin (ECH)

- Thailand is the major supplier, but we also started supplying to the local manufacturer and gradually our market share is also growing

- We have already started selling in Europe. And the US, our first vessel has reached in this month

– CPVC

- CPVC, the Indian market is almost around 2,25,000 tonnes per annum and which is growing almost at double digit

- This is the market of India and Indian manufacturing capacity is only 40 KTPA right now

– Chlorotoluene

- Chlorotoluene is mainly for the specialty

- There our customers will be the specialty chemical companies like all custom-manufacturing companies who are doing custom manufacturing for the multinational agrochemicals or the pharmaceutical companies

- This is the first time-in-India plant and we are planning 50% domestic market, all the specialty companies and 50% will be the export market

- Chlorotoluene definitely will start revenue from FY25 onwards slowly and gradually

– CAPEX

- In Q1 FY24, we spent Rs. 108 crores on our CAPEX plan

- We are on schedule for our expansions of CPVC of 45,000 tonnes per annum and chlorotoluene value chain and this will drive volume growth in FY25

– Debt

- Net debt as on 30th June 2023 is Rs. 902 crores as compared to Rs. 863 crores as on 31st March 2023

- The debt level, therefore, would remain around the same or just slightly below than what it has been in the previous year

– Guidance

- With regard to the absolute EBITDA for the FY24, this may be in the range of Rs. 450 crores to 500 crores

- Normally on a longer-term point of view, we believe that we will achieve those numbers – Rs. 5,000 crores – based on our expansion plan and the CAPEX plan

- We don’t give product-to-product margin, but whenever we select any product, our margin revolves around 25% to 28% and ROCE of around 25 or above that

(End)

Disclaimer: This is not a recommendation to buy/sell Epigral. The securities quoted are for illustration only and are not recommendatory.

Best Regards,

Ekansh Mittal

Research Analyst

Web: (opens in new tab)https://www.katalystwealth.

SEBI Research Analyst Registration No. INH100001690

Research Analyst Details

Name: Ekansh Mittal Email Id: (opens in new tab)[email protected] Ph: +91 727 5050062

Details of Associate: Not Applicable

Analyst Certification: The Analyst certify (ies) that the views expressed herein accurately reflect his (their) personal view(s) about the subject security (ies) and issuer(s) and that no part of his (their) compensation was, is or will be directly or indirectly related to the specific recommendation(s) or views contained in this research report.

Disclaimer: (opens in new tab)http://www.

Address – 7, Panch Ratan, 7/128, Swaroop Nagar, Kanpur – 208002, Contact No. – +91-7275050062

Compliance Officer – Mr. Ekansh Mittal, +91-9818866676, (opens in new tab)ekansh@

Grievance Redressal – Mittal Consulting, (opens in new tab)grievances@

“Registration granted by SEBI and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors”.

“Investment in securities market are subject to market risks. Read all the related documents carefully before investing.”

The views expressed are based solely on information available publicly and believed to be true. Investors are advised to independently evaluate the market conditions/risks involved before making any investment decision

This report is for the personal information of the authorized recipient and does not construe to be any investment, legal or taxation advice to you. Ekansh Mittal/Mittal Consulting/Katalyst Wealth is not soliciting any action based upon it. This report is not for public distribution and has been furnished to you solely for your information and should not be reproduced or redistributed to any other person in any form. This document is provided for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision. Ekansh Mittal or any of its affiliates or employees shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. Neither Ekansh Mittal, nor its employees, agents nor representatives shall be liable for any damages whether direct or indirect, incidental, special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information. Ekansh Mittal/Mittal Consulting or any of its affiliates or employees do not provide, at any time, any express or implied warranty of any kind, regarding any matter pertaining to this report, including without limitation the implied warranties of merchantability, fitness for a particular purpose, and non-infringement.

The recipients of this report should rely on their own investigations. Ekansh Mittal/Mittal Consulting and/or its affiliates and/or employees may have interests/ positions, financial or otherwise in the securities mentioned in this report. Mittal Consulting has incorporated adequate disclosures in this document. This should, however, not be treated as endorsement of the views expressed in the report.

We submit that no material disciplinary action has been taken on Ekansh Mittal by any regulatory authority impacting Equity Research Analysis.

Disclaimer: You can access it here – (opens in new tab)LINK

Whether the research analyst or research entity or his associate or his relative has any financial interest in the subject company/companies and the nature of such financial interest – No

Whether the research analyst or research entity or his associates or his relatives have actual/beneficial ownership of 1% or more securities of the subject company (at the end of the month immediately preceding the date of publication of the research report or date of the public appearance) – No

Whether the research analyst or research entity or his associate or his relative has any other material conflict of interest at the time of publication of the research report or at the time of public appearance – No

Whether it or its associates have received any compensation from the subject company in the past twelve months – No

Whether it or its associates have managed or co-managed public offering of securities for the subject company in the past 12 months – No

Whether it or its associates have received any compensation for investment banking or merchant banking or brokerage services from the subject company in the past 12 months – No

Whether it or its associates have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company in the past 12 months – No

Whether the subject company is or was a client during twelve months preceding the date of distribution of the research report and the types of services provided – No

Whether the research analyst has served as an officer, director or employee of the subject company – No

Whether the research analyst or research entity has been engaged in market making activity for the subject company – No