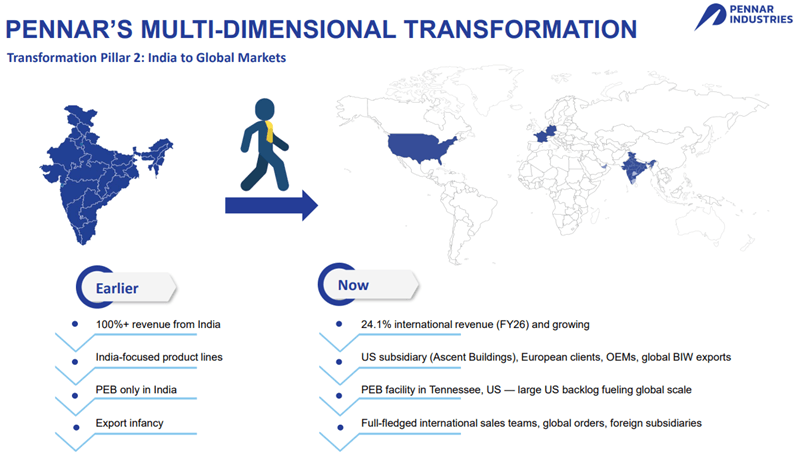

Most people tracking Indian capital goods stocks know the PEB (pre-engineered buildings) names. Fewer are watching Pennar Industries — which now generates 24% of its revenue from the US, runs plants in Tennessee and Alabama, and just committed to 20% PAT growth for FY27.

Here are my notes, but before that:

Help us grow: If you think our stock recommendations could add value to your friends, relatives, or acquaintances, we’d appreciate you spreading the word about Katalyst Wealth.

Latest Stock recommendations for Premium Members:

- Alpha & Alpha+ (Released: 2nd Jun ’26) A first-mover in a $7 billion global recycling opportunity — with proprietary technology that addresses a problem no one has cleanly solved yet. (opens in new tab)Read the full recommendation →

- Alpha+ (Released: 11th May ’26) A special situation with a 1–2 month holding period. ~14% upside from recommended levels (assuming full acceptance), and the stock needs to fall 10%+ before investors start losing money. (opens in new tab)Access this idea by signing up →

- Insider Bets (Released: 19th Apr ’26) A rare setup: promoter buying more via preferential allotment, valuations under 10x earnings and 1x book, and 20%+ earnings CAGR. Three green flags in one stock. (opens in new tab)See the full report by signing up →

Pennar Industries Q4 & FY26 concall notes

Financials at a glance

- ROCE: 20.23% | ROE: ~12%

- FY26 Total Income: ₹3,666 Cr (+12.35% YoY)

- FY26 EBITDA: ₹401 Cr (+15.51% YoY); EBITDA margin 11.09%

- FY26 PAT: ₹138.83 Cr (+16.22% YoY); PAT margin 3.83% vs 3.70% in FY25

- FY26 EPS: ₹10.29 vs ₹8.84

- Q4 PAT: ₹41.04 Cr (+14.89% YoY); Q4 PAT margin 4.44%

Business-wise order book (as of concall date)

- Hydraulics: ₹34 Cr (up from ₹22 Cr last quarter)

- PEB India: ₹810 Cr

- PEB US (incl. Ascent Structural): ~$63 Mn

- Boilers & Process Equipment: ₹145 Cr

PEB India

- Capacity utilisation at 70%; targeting 80% in FY27

- Labor issues fully resolved; recently declined a ₹150 Cr order on product mix grounds

- Double-digit revenue growth expected this year

PEB US

- Strong double-digit growth; demand driven by data centers, warehouses, industrial

- Order backlog up ~20% in the last three months

- Currently serving only South/Midwest — East and West Coast remain untapped

Engineering Services

- Outperformed in Q4; billing is entirely project-outcome based (not man-hours), so AI adoption improves margins

- US and Europe are key target markets; management targeting ₹100 Cr+ revenue in FY27

Boilers

- Secured largest-ever orders: 100 TPH AFBC + 80 TPH WHR boilers

- Called out as a “major growth lever” for FY27

Hydraulics

- Exploring Europe for new customers; modest contribution expected

- US tariff impact has moderated; order flow resuming

Margin trajectory

PAT margins have compounded from ~2% to 3.83% over four years, driven by mix shift toward PEB US, Engineering Services, and Boilers. ~30-35% of revenue is still legacy (low-growth, no fresh capital deployment); the remaining 65-70% is growing faster. Management guided for continued gradual improvement — no commitment to a big jump in FY27.

FY27 guidance

- PAT growth of 20% — firm management commitment

- Capex: ~₹100 Cr (BIW Hyundai plant + automation)

- Finance cost: below 4% of revenue

- Debt-to-equity: target 0.8x by year-end

As always, this is not a stock recommendation — This note is for informational purposes only and not a buy/sell recommendation. Please do your own due diligence before investing.

Hope you found the blog post useful and it added value to your investment decisions. Sign up for more interesting stock ideas and industry notes.

Not a research subscriber yet?

If you found this useful, our paid members get full research reports with entry levels, financial models, and entry-exit updates on stocks like these.

(opens in new tab)Explore Katalyst Wealth subscriptions →

Disclaimer: This is not a recommendation to buy/sell any of the stocks mentioned above. The securities quoted are for illustration only and are not recommendatory.

Ekansh Mittal

Research Analyst

SEBI Research Analyst Registration No. INH100001690

Research Analyst Details

Name: Ekansh Mittal Email Id: (opens in new tab)[email protected] Ph: +91 727 5050062

Details of Associate: Not Applicable

Analyst Certification: The Analyst certify (ies) that the views expressed herein accurately reflect his (their) personal view(s) about the subject security (ies) and issuer(s) and that no part of his (their) compensation was, is or will be directly or indirectly related to the specific recommendation(s) or views contained in this research report.

Disclaimer: (opens in new tab)http://www.

Registered Address – 7, Panch Ratan, 7/128, Swaroop Nagar, Kanpur – 208002

Place of Business – 205, Ratan Floor, 113/120, Swaroop Nagar, Kanpur – 208002

Compliance Officer/Grievance Redressal – Mr. Ekansh Mittal, +91-9818866676, (opens in new tab)info@

“Registration granted by SEBI and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors”.

“Investment in securities market are subject to market risks. Read all the related documents carefully before investing.”

The views expressed are based solely on information available publicly and believed to be true. Investors are advised to independently evaluate the market conditions/risks involved before making any investment decision

This report is for the personal information of the authorized recipient and does not construe to be any investment, legal or taxation advice to you. Ekansh Mittal/Mittal Consulting/Katalyst Wealth is not soliciting any action based upon it. This report is not for public distribution and has been furnished to you solely for your information and should not be reproduced or redistributed to any other person in any form. This document is provided for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision. Ekansh Mittal or any of its affiliates or employees shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. Neither Ekansh Mittal, nor its employees, agents nor representatives shall be liable for any damages whether direct or indirect, incidental, special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information. Ekansh Mittal/Mittal Consulting or any of its affiliates or employees do not provide, at any time, any express or implied warranty of any kind, regarding any matter pertaining to this report, including without limitation the implied warranties of merchantability, fitness for a particular purpose, and non-infringement.

The recipients of this report should rely on their own investigations. Ekansh Mittal/Mittal Consulting and/or its affiliates and/or employees may have interests/ positions, financial or otherwise in the securities mentioned in this report. Mittal Consulting has incorporated adequate disclosures in this document. This should, however, not be treated as endorsement of the views expressed in the report.

We submit that no material disciplinary action has been taken on Ekansh Mittal by any regulatory authority impacting Equity Research Analysis.

Use of Artificial Intelligence: RA may infrequently use Artificial Intelligence (AI) tools like chatgpt, notebooklm, etc. in its research services to enhance the quality and efficiency of the recommendations provided to clients. The tools are primarily used for data collection and generating con-call summaries for the purpose of research.

In accordance with Regulation 24(7) of the SEBI (Research Analyst) Regulations, 2014: We take full responsibility for the security, confidentiality, and integrity of client data used in conjunction with AI tools and we ensure compliance with applicable laws regarding the use of AI tools.

Disclaimer: You can access it here – (opens in new tab)LINK

Whether the research analyst or research entity or his associate or his relative has any financial interest in the subject company/companies and the nature of such financial interest – No

Whether the research analyst or research entity or his associates or his relatives have actual/beneficial ownership of 1% or more securities of the subject company (at the end of the month immediately preceding the date of publication of the research report or date of the public appearance) – No

Whether the research analyst or research entity or his associate or his relative has any other material conflict of interest at the time of publication of the research report or at the time of public appearance – No

Whether it or its associates have received any compensation from the subject company in the past twelve months – No

Whether it or its associates have managed or co-managed public offering of securities for the subject company in the past 12 months – No

Whether it or its associates have received any compensation for investment banking or merchant banking or brokerage services from the subject company in the past 12 months – No

Whether it or its associates have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company in the past 12 months – No

Whether the subject company is or was a client during twelve months preceding the date of distribution of the research report and the types of services provided – No

Whether the research analyst has served as an officer, director or employee of the subject company – No

Whether the research analyst or research entity has been engaged in market making activity for the subject company – No