Dear Members,

As mentioned in our Alpha Weekly update for 22nd Jan’12, the results season has begun and the first company (amongst the Alpha Recommendations) to announce its results is Cera Sanitaryware Ltd (NSE Code CERA).

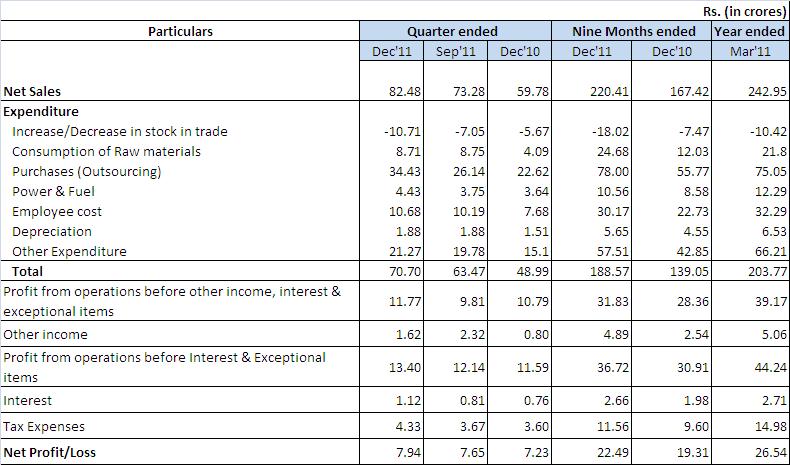

The results of Cera Sanitaryware are of significant importance to us as we have suggested the highest portfolio allocation (more than 10%) and we are happy to announce that the company has performed as per our expectations.

As can be observed from the above illustration, Cera has recorded a sharp 38% increase in net sales on YOY basis (Dec’11 against Dec’10 quarter). Even on sequential basis (QOQ – Dec’11 against Sep’11), the company has recorded a 12.5% growth in net sales at Rs 82.48 crore. Though, the industry leader, HSIL (Hindware) has not yet announced its Dec’11 results, we don’t expect HSIL to match up 38% growth in their “Building products” sales.

As was expected, the growth in profits has not kept pace with growth in sales. The EBITDA margins of the company have suffered on account of high cost of goods sold and increase in other expenditures. During the Oct-Dec’11 quarter, Cera embarked on an aggressive Print and Electronic media campaign. The company could have easily recorded better profitability, however it’s good to see that management is thinking in terms of long term benefits by spending money on creation and sustenance of brand equity. The EBITDA margins (inclusive of other income) of the company for the quarter ending Dec’11 stand at 18.18%, against 21.61% for Dec’10 and 18.54% for Sep’11.

For the nine months ending Dec’11, the company has recorded a sales turnover of Rs 220.41 crore, thus registering a growth of 31.65% against average industry growth of 15%. The growth in net profits is slightly lower at 16.5%, with 22.49 crore net profit for the nine months ending Dec’11.

We expect the margins of the company to improve from here on, as the inflation seems to have peaked during the Oct-Dec’11 quarter. Further, the rupee has recovered slightly against the dollar and the RBI has hinted towards lower policy rates in future.

For the entire FY 2012, we expect the company to close the year with a turnover of Rs 320 crore and a net profit of Rs 31-32 crore, thus a growth of 18-20% over FY 2011. The stock is currently available at 7-7.25 times FY 12 (E) earnings, while if one is to consider the business, performance, management, etc. it comes across as one of the best companies.

We believe Cera Sanitaryware is one of the best long term investment (3-4 years and more) opportunity that can compund one’s wealth at 30%+ (considering both the earnings and PE multiple expansion) for the next many years.

Disclaimer: We ourselves and our members at Katalysrt Wealth are invested in Cera Sanitaryware and therefore have a vested interest. Please carry out your own due diligence

Best Regards,

Ekansh Mittal

https://www.katalystwealth.com/

Ph.: 0120-4109766, Mob: +91-9818866676

Email:[email protected]