As the saying goes, the best time to study businesses is when the market isn’t rewarding them.

With broader markets down significantly from their highs, several quality mid and small cap names are trading at valuations that were hard to find even a year ago. One such business we’ve been tracking closely is Rajratan Global Wire, which just reported its strongest-ever quarter.

Here are the key takeaways, But, before that:

Help us grow: If you think our stock recommendations could add value to your friends, relatives, or acquaintances, we’d appreciate you spreading the word about Katalyst Wealth.

Also, here’s the list of new stock recommendations released in last few weeks:

- For Alpha/Alpha + members – On 22nd Mar’26, we released a new long term investment recommendation for (opens in new tab)Alpha and Alpha + members. Company has a Strong niche in rail‑centric infra (bridges, sleepers, signalling) with a large order book and strong balance sheet with good multi‑year growth visibility. Current mid‑teens P/E provide strong margin of safety. You can access it by signing up (opens in new tab)HERE

- For Insider Bets members – On 22nd Jan’26, we released our New stock report under “(opens in new tab)Insider Bets“ subscription. It’s a rare setup wherein Promoter is increasing stake via open market + preferential allotment, Valuations very reasonable at <10x earnings | <1x book and Earnings growth strong at 15%+ CAGR. You can access it by signing up (opens in new tab)HERE

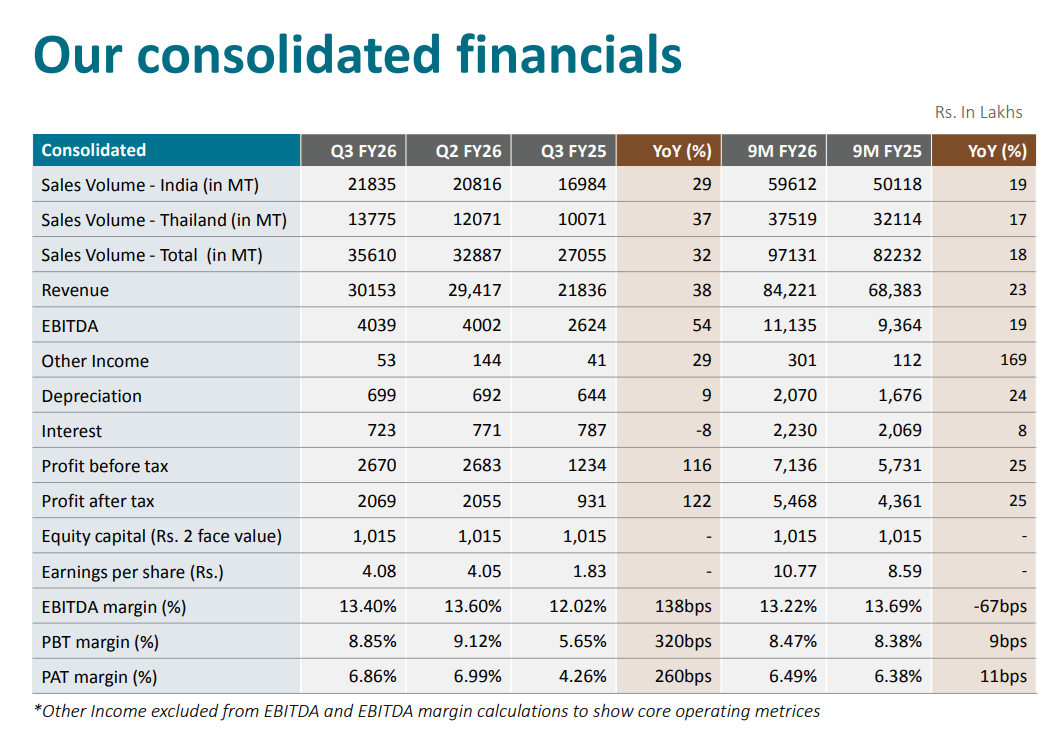

Rajratan Global Wire – Q2 FY26 Concall Takeaways: Inflection Point?

Q2 FY26 Performance

- Revenue growth of 20% YoY; quarterly volumes crossed 32,000 tons for the first time ever

- EBITDA close to Rs. 40 crore — highest ever in a single quarter

- Management called this the beginning of a “U-turn” after the subdued Q1

Chennai Plant — The Growth Engine

- Q2 Chennai sales: 4,768 MT vs Q1’s 2,485 MT — nearly doubled sequentially

- ~50% of South Indian customer volumes have already shifted from Indore to Chennai

- Chennai has turned monthly profitable

- Company has approved Rs. 20-25 crore CAPEX to expand Chennai to 60,000 tons capacity

- Equipment to arrive from Q1 FY27; no fresh customer approvals needed since it’s the same site

- Chennai exports for FY26 expected at ~6,000-7,000 tons

- Business with top 4-5 Chennai-proximate customers has grown 10-20% YoY

- Fixed cost at Chennai: Rs. 2.33 crore/month; 180 employees currently, to scale to 210 at full capacity

- Chennai depreciation providing income tax savings this year

Thailand — Running Hot at 91% Utilization

- Customer mix improving — higher proportion of sales now going to premium MNC customers, which is the key driver behind better realizations

- De-bottlenecking underway to squeeze out ~10% more capacity; no further expansion possible at current site

- Strategy: shift volumes from low-priced Chinese customers to higher-paying multinationals as approvals come through

- Chinese competition remains intense but Rajratan is profitably competing and growing

- No adverse impact from US reciprocal tariffs — bead wire falls under Section 232, excluded from bilateral trade negotiations

Exports — Scaling Up Fast

- Current run-rate: ~2,200-2,300 tons/month (1,200 from Thailand + 1,000 from India)

- FY26 total exports expected: ~20,000 tons

- FY27 target: 35,000-40,000 tons

- Markets: Southeast Asia (Sri Lanka, Indonesia, Malaysia, Vietnam), Europe, North America, Latin America; Japan being evaluated

- At one Japanese MNC in Europe, Rajratan is approved but supplying only 5-8% of their 3,000-4,000 tons/month requirement — significant headroom

- Korea focus de-prioritized due to proximity to China and slow approval scaling; growth trajectory shifting to Europe and America instead

- Working capital days have increased from ~70 to ~90 days purely due to longer export credit cycles (120-150 days for US shipments)

Wire Rope — The New Bet

- Pilot project: 10,000 tons/year capacity at Pithampur

- Total CAPEX: Rs. 70 crore; Rs. 29 crore already invested

- Production expected to start Q1 FY27

- Target EBITDA margin: 17-18%

- Approval cycles much shorter than bead wire (engineering product, not auto)

- US alone imports ~15,000 tons of wire rope every month — large addressable market

- Realization: ~Rs. 1,50,000 per ton vs ~Rs. 88,000-90,000 for bead wire

Competition & Moats

- Indian bead wire market: ~1,60,000-1,70,000 tons; installed capacity higher but viable (approved) capacity is the real constraint

- At current prices, plants need 60-65% utilization to break even; some competitors running at just 15%

- BIS approval remains a barrier for Chinese imports into India — even Rajratan Thailand’s BIS license is still pending despite inspection being done

- China has removed export rebate on bead wire (still exists on steel cord)

- Tata Steel, Aarti Steel, and Bansal Wires have added capacity, but Rajratan’s long presence, product quality, and strategic locations (Chennai + Indore) keep it ahead

- Steel tyre cord: management not entering this segment without a very strong partner — high investment, long approval cycles, and their own analysis doesn’t support the claimed 20% margins

PLI Update

- Chennai could not meet the committed 14,000-ton production target

- Applied for revision in year-on-year production targets; awaiting government approval

- If approved, 8% incentive on incremental sales would be entirely incremental to margins

- Not included in any current projections

Management Guidance & 3-Year Vision

- FY26-FY27: 15-20% volume growth each year; similar top-line growth

- EBITDA margins guided at 13-15%; beyond 15% requires a tailwind

- Realizations: India ~Rs. 88,000-90,000/ton; Thailand ~Rs. 80,000-83,000/ton

- Price range across customer types: $800 (Chinese customers) to $1,050 (premium European/North American) — a 25-30% gap

- 3-year vision: 1,80,000 tons of bead wire + 15,000-20,000 tons of other products (including wire rope) = ~2,00,000 tons total; top line of Rs. 1,800-2,000 crore

- FY27 CAPEX expected to be only Rs. 20-25 crore (maintenance + balancing equipment)

Fixed Cost Structure (Monthly)

- Indore: Rs. 4.55 crore/month (Rs. 8,000/ton at current volumes); 250 employees

- Chennai: Rs. 2.33 crore/month (per-ton cost still high due to low volumes, expected to drop significantly with ramp-up); 180 employees

- Both figures include employee costs, interest, depreciation, and overheads

Key Monitorables Going Forward

- PLI approval outcome

- Chennai volume ramp-up and per-ton cost reduction trajectory

- Export progression toward 40,000 tons in FY27

- Thailand customer mix shift from Chinese to premium MNC accounts

- Wire rope project commissioning and early market reception in Q1 FY27

We closely track high quality, strong growth companies with reasonable valuations as part of our research process at (opens in new tab)Alpha/Alpha +.

Hope you found the blog post useful and it added value to your investment decisions. Sign up for more interesting stock ideas and industry notes.

Disclaimer: This is not a recommendation to buy/sell any of the stocks mentioned above. The securities quoted are for illustration only and are not recommendatory.

Ekansh Mittal

Research Analyst

SEBI Research Analyst Registration No. INH100001690

Research Analyst Details

Name: Ekansh Mittal Email Id: (opens in new tab)[email protected] Ph: +91 727 5050062

Details of Associate: Not Applicable

Analyst Certification: The Analyst certify (ies) that the views expressed herein accurately reflect his (their) personal view(s) about the subject security (ies) and issuer(s) and that no part of his (their) compensation was, is or will be directly or indirectly related to the specific recommendation(s) or views contained in this research report.

Disclaimer: (opens in new tab)http://www.

Registered Address – 7, Panch Ratan, 7/128, Swaroop Nagar, Kanpur – 208002

Place of Business – 205, Ratan Floor, 113/120, Swaroop Nagar, Kanpur – 208002

Compliance Officer/Grievance Redressal – Mr. Ekansh Mittal, +91-9818866676, (opens in new tab)info@

“Registration granted by SEBI and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors”.

“Investment in securities market are subject to market risks. Read all the related documents carefully before investing.”

The views expressed are based solely on information available publicly and believed to be true. Investors are advised to independently evaluate the market conditions/risks involved before making any investment decision

This report is for the personal information of the authorized recipient and does not construe to be any investment, legal or taxation advice to you. Ekansh Mittal/Mittal Consulting/Katalyst Wealth is not soliciting any action based upon it. This report is not for public distribution and has been furnished to you solely for your information and should not be reproduced or redistributed to any other person in any form. This document is provided for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision. Ekansh Mittal or any of its affiliates or employees shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. Neither Ekansh Mittal, nor its employees, agents nor representatives shall be liable for any damages whether direct or indirect, incidental, special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information. Ekansh Mittal/Mittal Consulting or any of its affiliates or employees do not provide, at any time, any express or implied warranty of any kind, regarding any matter pertaining to this report, including without limitation the implied warranties of merchantability, fitness for a particular purpose, and non-infringement.

The recipients of this report should rely on their own investigations. Ekansh Mittal/Mittal Consulting and/or its affiliates and/or employees may have interests/ positions, financial or otherwise in the securities mentioned in this report. Mittal Consulting has incorporated adequate disclosures in this document. This should, however, not be treated as endorsement of the views expressed in the report.

We submit that no material disciplinary action has been taken on Ekansh Mittal by any regulatory authority impacting Equity Research Analysis.

Use of Artificial Intelligence: RA may infrequently use Artificial Intelligence (AI) tools like chatgpt, notebooklm, etc. in its research services to enhance the quality and efficiency of the recommendations provided to clients. The tools are primarily used for data collection and generating con-call summaries for the purpose of research.

In accordance with Regulation 24(7) of the SEBI (Research Analyst) Regulations, 2014: We take full responsibility for the security, confidentiality, and integrity of client data used in conjunction with AI tools and we ensure compliance with applicable laws regarding the use of AI tools.

Disclaimer: You can access it here – (opens in new tab)LINK

Whether the research analyst or research entity or his associate or his relative has any financial interest in the subject company/companies and the nature of such financial interest – No

Whether the research analyst or research entity or his associates or his relatives have actual/beneficial ownership of 1% or more securities of the subject company (at the end of the month immediately preceding the date of publication of the research report or date of the public appearance) – No

Whether the research analyst or research entity or his associate or his relative has any other material conflict of interest at the time of publication of the research report or at the time of public appearance – No

Whether it or its associates have received any compensation from the subject company in the past twelve months – No

Whether it or its associates have managed or co-managed public offering of securities for the subject company in the past 12 months – No

Whether it or its associates have received any compensation for investment banking or merchant banking or brokerage services from the subject company in the past 12 months – No

Whether it or its associates have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company in the past 12 months – No

Whether the subject company is or was a client during twelve months preceding the date of distribution of the research report and the types of services provided – No

Whether the research analyst has served as an officer, director or employee of the subject company – No

Whether the research analyst or research entity has been engaged in market making activity for the subject company – No