Most investors look at a PAT number and move on. The investors who find compounders early read the footnotes.

MMP Industries just reported its highest-ever quarterly and full-year revenue — and buried inside the numbers are three businesses nobody is talking about yet.

Here are my notes, but before that:

Help us grow: If you think our stock recommendations could add value to your friends, relatives, or acquaintances, we’d appreciate you spreading the word about Katalyst Wealth.

Latest Stock recommendations for Premium Members:

- Insider Bets (Released: 8th Jul ’26) A rare setup: Promoter increasing stake + business transformation + Reasonable valuations. Three green flags in one stock. (opens in new tab)Read the full recommendation →

- Alpha+ (Released: 29th Jun ’26) A special situation with a 1–2 month holding period. ~11% upside from recommended levels (assuming full acceptance), and the stock needs to fall 16%+ before investors start losing money. (opens in new tab)Access this idea by signing up →

- Alpha & Alpha+ (Released: 2nd Jun ’26) A first-mover in a $7 billion global recycling opportunity — with proprietary technology that addresses a problem no one has cleanly solved yet. (opens in new tab)Read the full recommendation →

MMP Industries – Notes from the Presentation + Concall

The company: MMP Industries Ltd (NSE: MMP) — a 40+ year old Nagpur-based aluminium manufacturer now expanding into polymer insulators, LT cables, and renewable energy. Market cap: ~₹732 Cr.

The headline numbers (FY26, Consolidated):

- PAT: ₹31 Cr — down 20% YoY, but here’s why that number is misleading

- Revenue: ₹824 Cr, up 19% YoY (4-year CAGR: 29%)

- EBITDA: ₹66 Cr, 8% margin

Why the PAT decline needs context:

MMP’s Umred facility caught fire in April 2025 — estimated ₹45-50 Cr revenue loss, ₹7-8 Cr EBITDA impact. Two new subsidiaries in ramp-up phase dragged EBITDA by another ₹4 Cr. Excluding these, PAT would have been ₹11-12 Cr higher. Normalised FY26 was materially stronger than reported numbers suggest.

Three businesses the market isn’t pricing in yet:

Polymer Insulators — ₹35-40 Cr invested, both phases fully operational, FY26 revenue just ₹2.3 Cr (still in approval stage). The concall numbers are striking: target EBITDA margin of ~20%, asset turn of ~3.5x, implying peak revenue potential of ₹130-140 Cr from existing capex. Management guided ₹18-20 Cr revenue in FY27, ₹45-50 Cr in FY28. Already approved with Adani Renewables; PGCIL and major EPC approvals expected Q2FY27. Exports to Nepal have commenced; RFQs from US and Latin America progressing.

LT Cables — ₹85-90 Cr greenfield capex planned over 2-2.5 years, pilot launch targeted June 2026. This is a step up the value chain from bare conductors — management guided 14-15% EBITDA margins vs the current ~5% in the conductors business. Backward integration into aluminium wire rods (₹13-15 Cr) planned alongside.

Solar Capex — 7 MW group captive solar park under development (₹30 Cr, commissioning H1FY27). Currently 20% of energy needs met in-house. Target: 40-50% renewable within 3-4 years. The investor angle: lower energy cost improves EBITDA per ton across every existing business — not just new ones.

The core businesses:

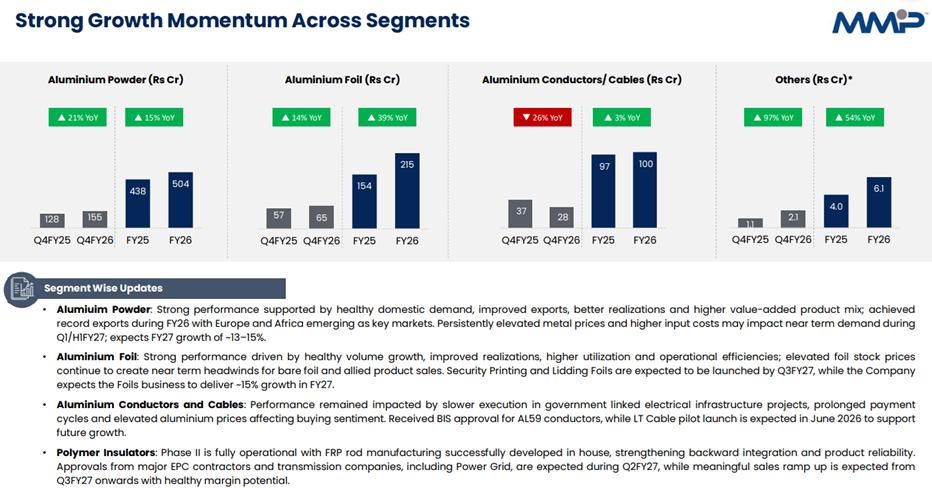

Aluminium Powders (61% of revenue, ₹504 Cr, up 15%) operating at ~80% utilization. Record exports to Europe and Africa — clients include UltraTech, Shree Cement, UPL, Sumitomo Chemical. No new capacity planned; management focused on shifting to higher value-added grades. EBITDA per ton: ₹37,000-42,000.

Aluminium Foils (26% of revenue, ₹215 Cr, up 39%) serving pharma packaging clients including Sun Pharma, Aurobindo, Intas, Torrent. Rolling mill at 80-85% utilization; conversion section at ~45-50% — that gap is the margin improvement runway. Security Printing and Lidding Foils launching Q3FY27.

The one thing from the concall most people will miss:

A long-standing investor asked point blank: “when are we going to get a respectable return on capital?” The CFO’s honest answer: ROCE of 13-14% in FY27, “more than 15%” in FY28 — still below cost of capital today.

Management’s case: foil startup losses are behind them, solar cuts energy costs, polymer insulators carry 20% margins, LT cables bring better realization. The pieces are in place — but FY27 is still an investment year, not a harvest year.

As always, this is not a stock recommendation — This note is for informational purposes only and not a buy/sell recommendation. Please do your own due diligence before investing.

Hope you found the blog post useful and it added value to your investment decisions. Sign up for more interesting stock ideas and industry notes.

Not a research subscriber yet?

If you found this useful, our paid members get full research reports with entry levels, financial models, and entry-exit updates on stocks like these.

(opens in new tab)Explore Katalyst Wealth subscriptions →

Disclaimer: This is not a recommendation to buy/sell any of the stocks mentioned above. The securities quoted are for illustration only and are not recommendatory.

Ekansh Mittal

Research Analyst

SEBI Research Analyst Registration No. INH100001690

Research Analyst Details

Name: Ekansh Mittal Email Id: (opens in new tab)[email protected] Ph: +91 727 5050062

Details of Associate: Not Applicable

Analyst Certification: The Analyst certify (ies) that the views expressed herein accurately reflect his (their) personal view(s) about the subject security (ies) and issuer(s) and that no part of his (their) compensation was, is or will be directly or indirectly related to the specific recommendation(s) or views contained in this research report.

Disclaimer: (opens in new tab)http://www.

Registered Address – 7, Panch Ratan, 7/128, Swaroop Nagar, Kanpur – 208002

Place of Business – 205, Ratan Floor, 113/120, Swaroop Nagar, Kanpur – 208002

Compliance Officer/Grievance Redressal – Mr. Ekansh Mittal, +91-9818866676, (opens in new tab)info@

“Registration granted by SEBI and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors”.

“Investment in securities market are subject to market risks. Read all the related documents carefully before investing.”

The views expressed are based solely on information available publicly and believed to be true. Investors are advised to independently evaluate the market conditions/risks involved before making any investment decision

This report is for the personal information of the authorized recipient and does not construe to be any investment, legal or taxation advice to you. Ekansh Mittal/Mittal Consulting/Katalyst Wealth is not soliciting any action based upon it. This report is not for public distribution and has been furnished to you solely for your information and should not be reproduced or redistributed to any other person in any form. This document is provided for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision. Ekansh Mittal or any of its affiliates or employees shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. Neither Ekansh Mittal, nor its employees, agents nor representatives shall be liable for any damages whether direct or indirect, incidental, special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information. Ekansh Mittal/Mittal Consulting or any of its affiliates or employees do not provide, at any time, any express or implied warranty of any kind, regarding any matter pertaining to this report, including without limitation the implied warranties of merchantability, fitness for a particular purpose, and non-infringement.

The recipients of this report should rely on their own investigations. Ekansh Mittal/Mittal Consulting and/or its affiliates and/or employees may have interests/ positions, financial or otherwise in the securities mentioned in this report. Mittal Consulting has incorporated adequate disclosures in this document. This should, however, not be treated as endorsement of the views expressed in the report.

We submit that no material disciplinary action has been taken on Ekansh Mittal by any regulatory authority impacting Equity Research Analysis.

Use of Artificial Intelligence: RA may infrequently use Artificial Intelligence (AI) tools like chatgpt, notebooklm, etc. in its research services to enhance the quality and efficiency of the recommendations provided to clients. The tools are primarily used for data collection and generating con-call summaries for the purpose of research.

In accordance with Regulation 24(7) of the SEBI (Research Analyst) Regulations, 2014: We take full responsibility for the security, confidentiality, and integrity of client data used in conjunction with AI tools and we ensure compliance with applicable laws regarding the use of AI tools.

Disclaimer: You can access it here – (opens in new tab)LINK

Whether the research analyst or research entity or his associate or his relative has any financial interest in the subject company/companies and the nature of such financial interest – No

Whether the research analyst or research entity or his associates or his relatives have actual/beneficial ownership of 1% or more securities of the subject company (at the end of the month immediately preceding the date of publication of the research report or date of the public appearance) – No

Whether the research analyst or research entity or his associate or his relative has any other material conflict of interest at the time of publication of the research report or at the time of public appearance – No

Whether it or its associates have received any compensation from the subject company in the past twelve months – No

Whether it or its associates have managed or co-managed public offering of securities for the subject company in the past 12 months – No

Whether it or its associates have received any compensation for investment banking or merchant banking or brokerage services from the subject company in the past 12 months – No

Whether it or its associates have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company in the past 12 months – No

Whether the subject company is or was a client during twelve months preceding the date of distribution of the research report and the types of services provided – No

Whether the research analyst has served as an officer, director or employee of the subject company – No

Whether the research analyst or research entity has been engaged in market making activity for the subject company – No