Dear Readers,

From our reading of the various journals and newsletters, we come across different stock ideas. The same acts as a good starting point for carrying out in-depth research on good stocks idea. Off-late we came across Bliss GVS Pharma as a stock recommendation in various journals and also on the leading business daily i.e. The Economic Times.

(Refer the link: https://articles.economictimes.indiatimes.com/2011-01-10/news/28432881_1_gvs-labs-brand-manufacturing).

The company is renowned for manufacturing and marketing a unique product ‘Today’ which is a Vaginal Contraceptive, a female contraceptive aimed at furthering planned parenthood.

We carried out some primary research at our end and this is to inform you that we would like to caution (all invested or contemplating investing) all against investing in Bliss GVS Pharma.

The numbers look dicey to us and through this post we would even suggest all readers to mandatorily check  the cash flows of the company, rather than just devoting complete attention on the reported earnings. After all, Cash is the ultimate king for any business.

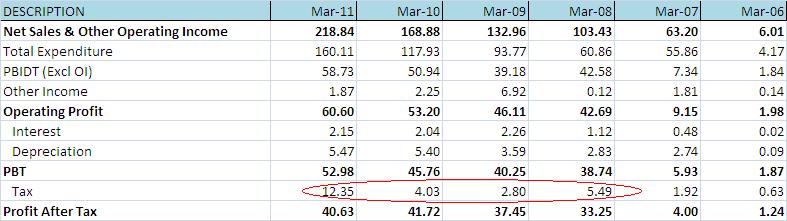

Reported earnings

On the face of it, the sales and earnings growth looks good. Since the company operates in Pharma space with negligible debt, one is bound to get interested about the stock. However, as highlighted above the tax outgo seems abysmally low and warrants a check. We consider taxes paid as an important metric. Let’s check the same and other important operational details with Cash Flow statement of the company.

Cash Flow statement

While the earnings statement of the company brings out a very rosy picture, the cash flows statement is portraying a completely different story and the same should bring on guard any prudent investor.

Some simple calculations tell us that while during the last 6 years the cumulative Profit after tax reported by the company is Rs 159 crore, the cumulative Cash flows from operations for the same period stand at Rs 48.65 crore.

Well, that’s a hell of a lot of difference. Occasional blip in cash flows is understandable, however such a huge difference is definitely alarming. Then what’s causing such a huge difference in reported earnings and the actual cash flows? Seems like a case of high working capital requirement. Balance sheet shall help us throw some light on the same.

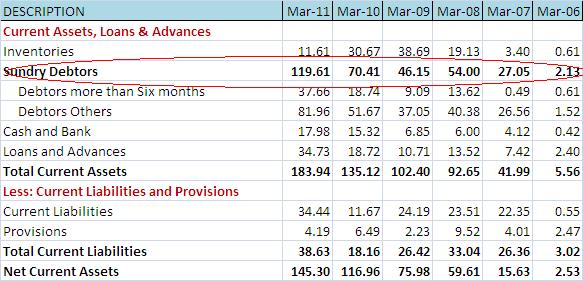

Balance Sheet

As can be observed above the Sundry debtors of the company is abnormally high, and rather growing at a rate higher than the net sales of the company. The same points towards very aggressive accounting practices of the company. At the same time, the company does not enjoy the same credit facility from its creditors with current liabilities remaining more or less same over the last 5 years.

We believe that the company could either be pushing very hard for it’s products or could even be cooking it’s books. In any case, the same does not send out a very good signal for the existing shareholders and the ones who are contemplating buying the stock of the company.

Ekansh Mittal [[email protected]]