Dear Sir,

Auto industry is going through one of its worst periods. The passenger vehicle sales are down significantly and even the 2W sales are down.

However, we are looking at this downturn more as an opportunity. A lot of really good companies in the auto-ancillary space are down 70-80% from their highs and are trading at historically low valuations.

We are therefore especially focused on auto components supplier and that too in 2W space. Another point that we are keeping in mind is that company’s products should not get disrupted by electric vehicle adoption and should rather benefit from the same.

Why 2W space? Because the history suggests that the slowdowns in the 2W segment are shorter (a year or so) and less pronounced.

Source: Edelweiss Automobiles Jul’19 report

Thus, keeping the above factors in mind, we recently shared an opportunity with all our premium members on a company that is segment leader, growing despite the slowdown and trading at historically low valuations. The new recommendation is also part of our Model portfolio of stocks.

If you missed investing during 2008-09, 2012-13 market corrections, you shouldn’t miss out on the latest opportunity the market is serving us in 2019. You can invest in our latest pick and make the most of it by subscribing to Premium Membership. Please register HERE

Some important points about the company are as below:

- The stock is down more than 75% from its highs

- The current valuations are historically low on almost all the parameters: less than 1 time book value, less than 9 times earnings, etc

- In the last 7 months the promoters have bought significant quantity from the market. Their average purchase price is around 25% higher than our recommendation price

- The company is the largest player in the segment and its clients account for more than 50% of the 2W sales in India

- Barring 1 year, the company has consistently outperformed 2W industry sales growth by a wide margin.

- The company has consistently clocked more than 15% growth in sales on year on year basis.

- Despite the slowdown in 2W volumes, the company is likely to sustain double digit growth rate on the back of 2-4x increase (over the years) in realizations in 50% of its product segment.

- The dividend yield is more than 2%

Stock market is peculiar…sometimes it is too exuberant and offers an asset worth Rs 100 at Rs 120-150 and sometimes it becomes too despondent and offers the same asset worth Rs 100 at Rs 40-60.

Our returns on investments are therefore determined by when we buy the stock: at 40-50 when the market is depressed or 120-150 when the market is elated.

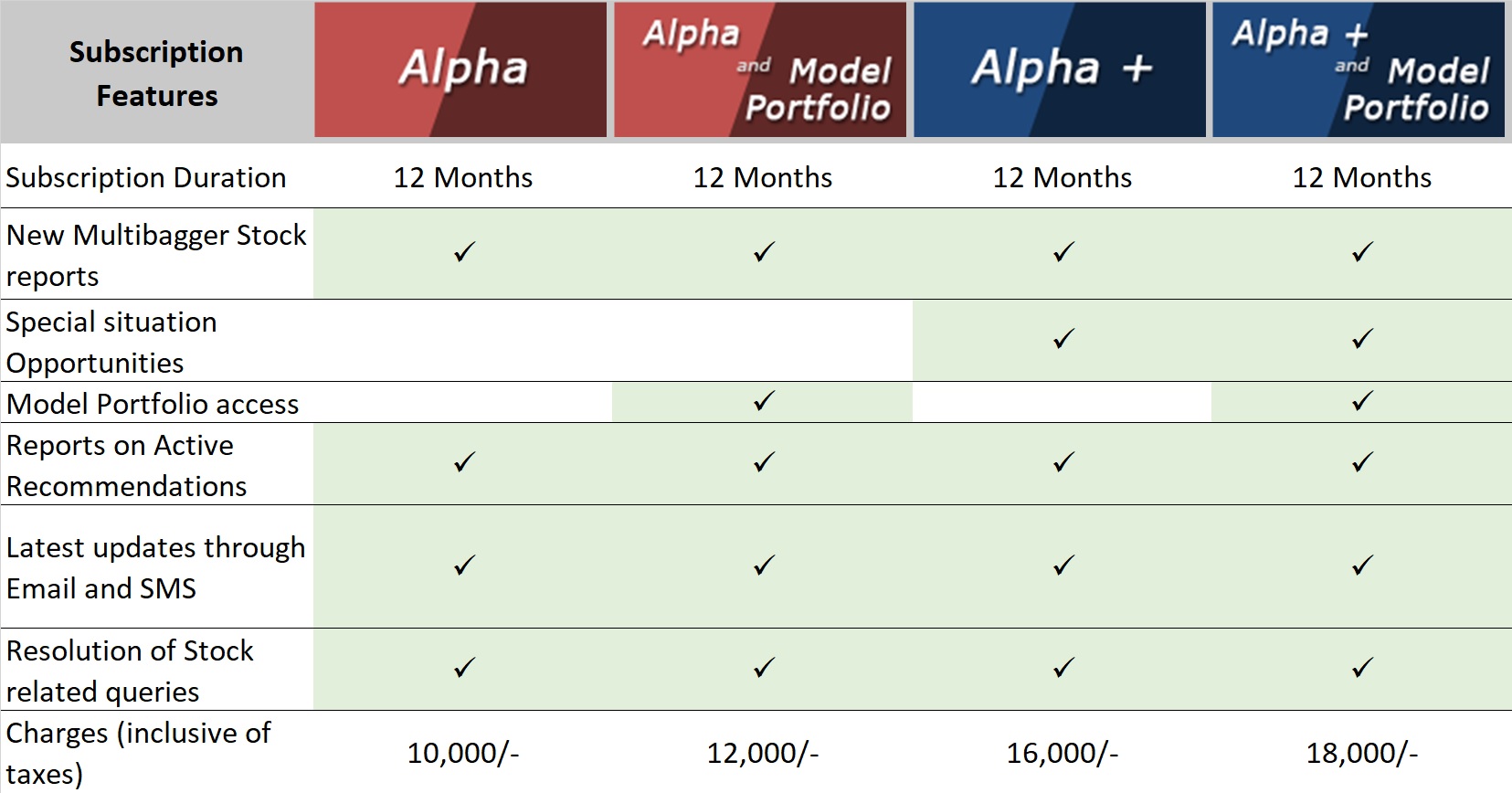

Get access to our latest pick by subscribing to one of our Premium Memberships. The new recommendation is also part of our Model Portfolio.

Premium Membership

We help our premium members create long term wealth through our stock recommendations, model portfolio, stock updates, etc. We are registered with SEBI and have been recognized by none other than Forbes and Economic Times (ET) for our stock research prowess. Below, you can read more about our service offerings to our members.

For more details – Click HERE

We strongly care for and look for association with like-minded clients and would like to extend our invitation to the investor:

- Who looks at ownership of stocks as partial ownership of businesses?

- Who is patient and serious about exploring high quality businesses?

- Who understands the fact that stock prices are the slave of earnings and sooner than later they start reflecting the same.

- Who doesn’t have a phobia of watching his stocks go down over the short term?

- Who is patient enough to hold a good undervalued stock for a period of 1 year and more?

- Who does not get enough time to research.

- Who researches and invests himself, however looking for a source of good research analysis on stocks.

SEBI Registration No. INH100001690

Ekansh Mittal

Research Analyst

Web: https://katalystwealth.com/

Email: [email protected]

Ph: +91-727-5050062, Mob: +91-9818866676

Rating Interpretation

Positive – Expected return of ~15% + on annualized basis in medium to long term for investment recommendations and in short term for Special situations

Neutral – Expected Absolute return in the range of +/- 15%

Negative – Expected Absolute return of over -15%

Coverage closure – No further update on the stock

% weightage – allocation in the subject stock with respect to equity investments

Short term – Less than 1 year

Medium term – Greater than 1 year and less than 3 years

Long term – Greater than 3 years

Research Analyst Details

Name: Ekansh Mittal Email Id: [email protected] Ph: +91 727 5050062

Analyst ownership of the stock: No

Details of Associates: Not Applicable

Analyst Certification: The Analyst certify (ies) that the views expressed herein accurately reflect his (their) personal view(s) about the subject security (ies) and issuer(s) and that no part of his (their) compensation was, is or will be directly or indirectly related to the specific recommendation(s) or views contained in this research report.

Disclaimer: www.katalystwealth.com (here in referred to as Katalyst Wealth) is the domain owned by Ekansh Mittal. Mr. Ekansh Mittal is the sole proprietor of Mittal Consulting and offers independent equity research services to retail clients on subscription basis. SEBI (Research Analyst) Regulations 2014, Registration No. INH100001690

The views expressed are based solely on information available publicly and believed to be true. Investors are advised to independently evaluate the market conditions/risks involved before making any investment decision

A graph of daily closing prices of securities is available at www.bseindia.com (Choose a company from the list on the browser and select the “three years” period in the price chart

This report is for the personal information of the authorized recipient and does not construe to be any investment, legal or taxation advice to you. Ekansh Mittal/Mittal Consulting/Katalyst Wealth is not soliciting any action based upon it. This report is not for public distribution and has been furnished to you solely for your information and should not be reproduced or redistributed to any other person in any form. This document is provided for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision. Ekansh Mittal or any of its affiliates or employees shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. Neither Ekansh Mittal, nor its employees, agents nor representatives shall be liable for any damages whether direct or indirect, incidental, special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information. Ekansh Mittal/Mittal Consulting or any of its affiliates or employees do not provide, at any time, any express or implied warranty of any kind, regarding any matter pertaining to this report, including without limitation the implied warranties of merchantability, fitness for a particular purpose, and non-infringement.

The recipients of this report should rely on their own investigations. Ekansh Mittal/Mittal Consulting and/or its affiliates and/or employees may have interests/ positions, financial or otherwise in the securities mentioned in this report. Mittal Consulting has incorporated adequate disclosures in this document. This should, however, not be treated as endorsement of the views expressed in the report.

We submit that no material disciplinary action has been taken on Ekansh Mittal by any regulatory authority impacting Equity Research Analysis.

Disclosure (SEBI RA Regulations)

Whether the research analyst or research entity or his associate or his relative has any financial interest in the subject company/companies and the nature of such financial interest – No

Whether the research analyst or research entity or his associates or his relatives have actual/beneficial ownership of 1% or more securities of the subject company (at the end of the month immediately preceding the date of publication of the research report or date of the public appearance) – No

Whether the research analyst or research entity or his associate or his relative has any other material conflict of interest at the time of publication of the research report or at the time of public appearance – No

Whether it or its associates have received any compensation from the subject company in the past twelve months – No

Whether it or its associates have managed or co-managed public offering of securities for the subject company in the past 12 months – No

Whether it or its associates have received any compensation for investment banking or merchant banking or brokerage services from the subject company in the past 12 months – No

Whether it or its associates have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company in the past 12 months – No

Whether the subject company is or was a client during twelve months preceding the date of distribution of the research report and the types of services provided – No

Whether the research analyst has served as an officer, director or employee of the subject company – No

Whether the research analyst or research entity has been engaged in market making activity for the subject company – No