Hello Sir,

Hope you are doing well.

Next 6-12 months look crucial from the view of wealth creation over the next 3-4 years.

As they say, it takes a prepared mind to capitalize on the opportunities and we have therefore intensified our research to identify potential investment opportunities.

Today, we would like to bring to your notice Apex Frozen foods and share notes from its latest presentation. Since the last few years the Shrimp industry hasn't done very well and the stocks are down 50-60% from their 2017 highs.

In general, we like looking at companies which have done well in the past but currently going through a tough phase as a lot of times one can get good companies at cheaper valuations in such scenarios.

Hope you find the details useful for your own investments or to add the stock to your watch list:

Before that, if you are interested in investing in our Latest Stock Recommendation which could benefit from the massive growth expected in the CNG segment and still available around 10 times earnings, you can read about it by Clicking HERE

Apex Frozen Jun'22 presentation

Company details -

- Commenced business operations in 1995, Apex Frozen Foods has grown to become one of the leading shrimp processors & exporters in India

- Diversified customer base of Food Companies, Retail Chains, Restaurants, Club Stores and Distributors across the key markets

- Well integrated operations with presence in Hatchery and Processing & Exporting of Shrimp

- FY 22 Geographical sales mix - 80% USA, 18% Europe and 2% China

- Hatcheries with a total current capacity of 1.2-1.4 bn Specific Pathogen Free (SPF) shrimp seed

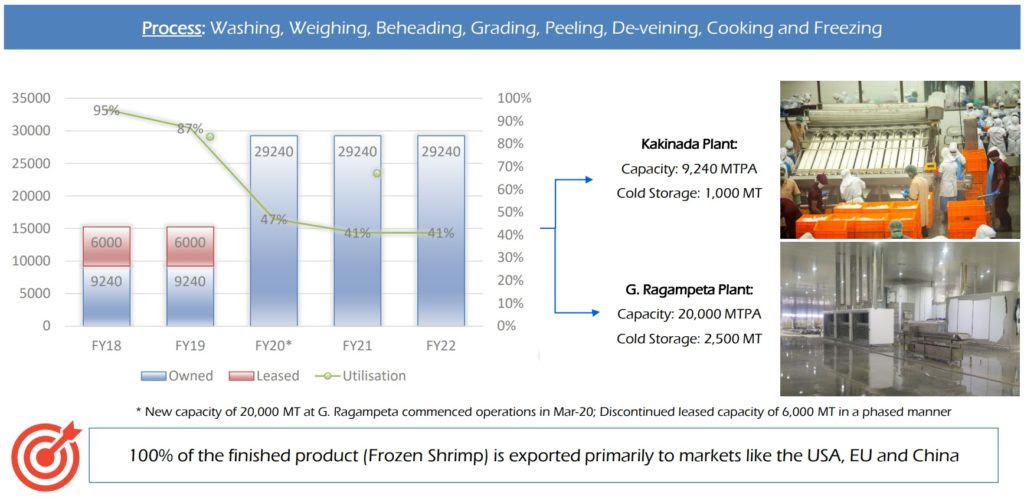

- Two facilities with a total Processing Capacity of 29,240 MTPA and Cold Storage capacity of ~3,500 MT

Processing Capacity - Of the 20,000 MTPA capacity at G. Ragampeta plant (commissioned in Mar-20), 5,000 MTPA is towards Ready-to-Eat (new product line)

Source: Apex Frozen Jun'22 presentation

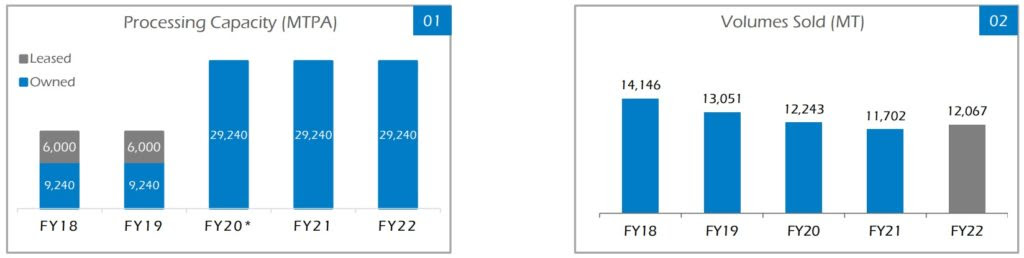

Capacity and volumes sold -

Source: Apex Frozen Jun'22 presentation

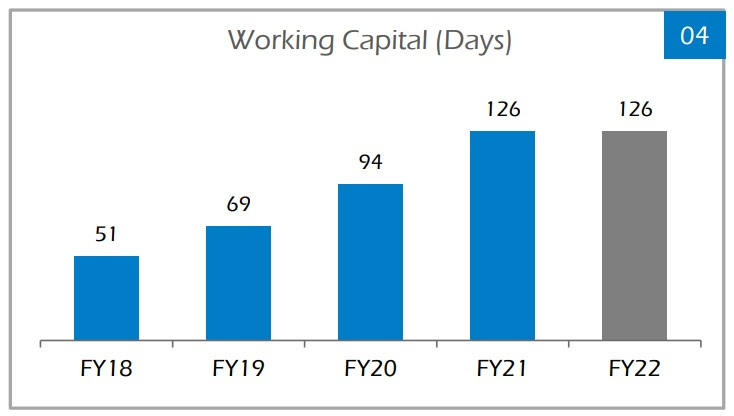

Working Capital Days - Working capital days increased due to enhanced Hatchery operations since FY19 and inventory & debtor build-up from FY20 end onwards, led by the Covid-19 impact

Source: Apex Frozen Jun'22 presentation

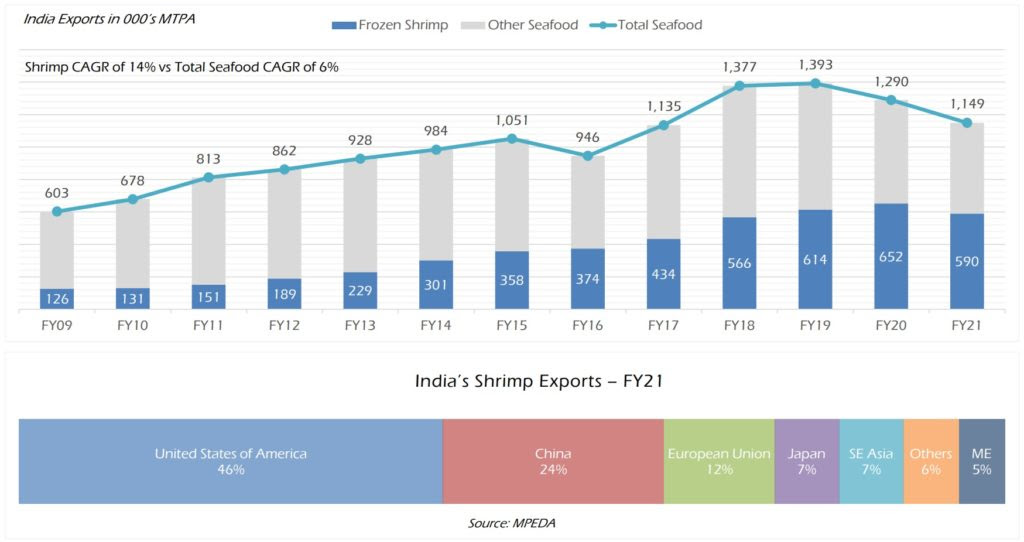

India Sea food exports -

Source: Apex Frozen Jun'22 presentation

FY 22 performance update -

- Overall capacity utilization remained flat YoY at ~41% in FY22 as the Company limited its production considering the prevailing sea transportation issues

- Shrimp sales volumes grew by 3% Y-o-Y to 12,067 MT in FY22 vs 11,702 MT in FY 21, with higher growth in Ready-To-Eat (RTE) products at 39% YoY to 2,364 MT

- The share of high value-added RTE products increased to ~20% in FY22 versus ~15% in FY21

- Approved capacity expansion of RTE products from 5,000 MTPA to 10,000 MTPA

Risks -

- Being an export-oriented sector, any slowdown in consumption in key markets like the USA, EU and South-East Asia will have an adverse impact on India’s shrimp exports

- Highly susceptible to outbreak of diseases, which can have a detrimental effect on the availability of raw material (shrimp)

Disclaimer: This is not a recommendation on the stock. These updates are as announced by the companies on exchanges and only for the purpose of information and education.

If you are looking for investment opportunities do check out our premium subscriptions. We have been helping our clients with our stock recommendations for over a decade now.

Best Regards,

Ekansh Mittal

Research Analyst

Web: https://www.katalystwealth.

SEBI Research Analyst Registration No. INH100001690

Research Analyst Details

Name: Ekansh Mittal Email Id: [email protected] Ph: +91 727 5050062

Details of Associate: Not Applicable

Analyst Certification: The Analyst certify (ies) that the views expressed herein accurately reflect his (their) personal view(s) about the subject security (ies) and issuer(s) and that no part of his (their) compensation was, is or will be directly or indirectly related to the specific recommendation(s) or views contained in this research report.

Disclaimer: http://www.

The views expressed are based solely on information available publicly and believed to be true. Investors are advised to independently evaluate the market conditions/risks involved before making any investment decision

This report is for the personal information of the authorized recipient and does not construe to be any investment, legal or taxation advice to you. Ekansh Mittal/Mittal Consulting/Katalyst Wealth is not soliciting any action based upon it. This report is not for public distribution and has been furnished to you solely for your information and should not be reproduced or redistributed to any other person in any form. This document is provided for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision. Ekansh Mittal or any of its affiliates or employees shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. Neither Ekansh Mittal, nor its employees, agents nor representatives shall be liable for any damages whether direct or indirect, incidental, special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information. Ekansh Mittal/Mittal Consulting or any of its affiliates or employees do not provide, at any time, any express or implied warranty of any kind, regarding any matter pertaining to this report, including without limitation the implied warranties of merchantability, fitness for a particular purpose, and non-infringement.

The recipients of this report should rely on their own investigations. Ekansh Mittal/Mittal Consulting and/or its affiliates and/or employees may have interests/ positions, financial or otherwise in the securities mentioned in this report. Mittal Consulting has incorporated adequate disclosures in this document. This should, however, not be treated as endorsement of the views expressed in the report.

We submit that no material disciplinary action has been taken on Ekansh Mittal by any regulatory authority impacting Equity Research Analysis.

Disclaimer: You can access it here - LINK

Whether the research analyst or research entity or his associate or his relative has any financial interest in the subject company/companies and the nature of such financial interest – No

Whether the research analyst or research entity or his associates or his relatives have actual/beneficial ownership of 1% or more securities of the subject company (at the end of the month immediately preceding the date of publication of the research report or date of the public appearance) – No

Whether the research analyst or research entity or his associate or his relative has any other material conflict of interest at the time of publication of the research report or at the time of public appearance – No

Whether it or its associates have received any compensation from the subject company in the past twelve months – No

Whether it or its associates have managed or co-managed public offering of securities for the subject company in the past 12 months – No

Whether it or its associates have received any compensation for investment banking or merchant banking or brokerage services from the subject company in the past 12 months – No

Whether it or its associates have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company in the past 12 months – No

Whether the subject company is or was a client during twelve months preceding the date of distribution of the research report and the types of services provided – No

Whether the research analyst has served as an officer, director or employee of the subject company – No

Whether the research analyst or research entity has been engaged in market making activity for the subject company – No