Most investors know Filatex India as a polyester yarn maker. Few know that it’s quietly building India’s first textile recycling plant on the side and has signed an MOU with Decathlon India.

Here are important details about textile recycling plant and potential profitability, but before that:

Help us grow: If you think our stock recommendations could add value to your friends, relatives, or acquaintances, we’d appreciate you spreading the word about Katalyst Wealth.

Latest recommendations shared with Alpha, Alpha + and Insider Bets members:

- For Insider Bets members – On 19th Apr’26, we released our New stock report under “(opens in new tab)Insider Bets“ subscription. It’s a rare setup wherein Promoter is increasing stake via preferential allotment, Valuations very reasonable at <10x earnings | 1x book and Earnings growth strong at 20%+ CAGR. You can access it by signing up (opens in new tab)HERE.

- For Alpha/Alpha + members – On 22nd Mar’26, we released a new long term investment recommendation for (opens in new tab)Alpha and Alpha + members. Company has a Strong niche in rail‑centric infra (bridges, sleepers, signalling) with a large order book and strong balance sheet with good multi‑year growth visibility. Current mid‑teens P/E provide strong margin of safety. You can access it by signing up (opens in new tab)HERE

Filatex India – Interesting details from Presentation

FY26 FINANCIALS (Standalone)

- Revenue: ₹4,160 Cr

- EBITDA: ₹346 Cr | Margin: 8.33% (+227 bps YoY)

- PAT: ₹183 Cr | Growth: +36.66% YoY

- ROCE: 14.90% | ROE: 12.96%

OPERATIONS

- Among Top 5 Polyester Filament Yarn (PFY) producers in India

- 4,17,240 TPA installed capacity, >90% utilisation

- Fully integrated melt-to-yarn value chain

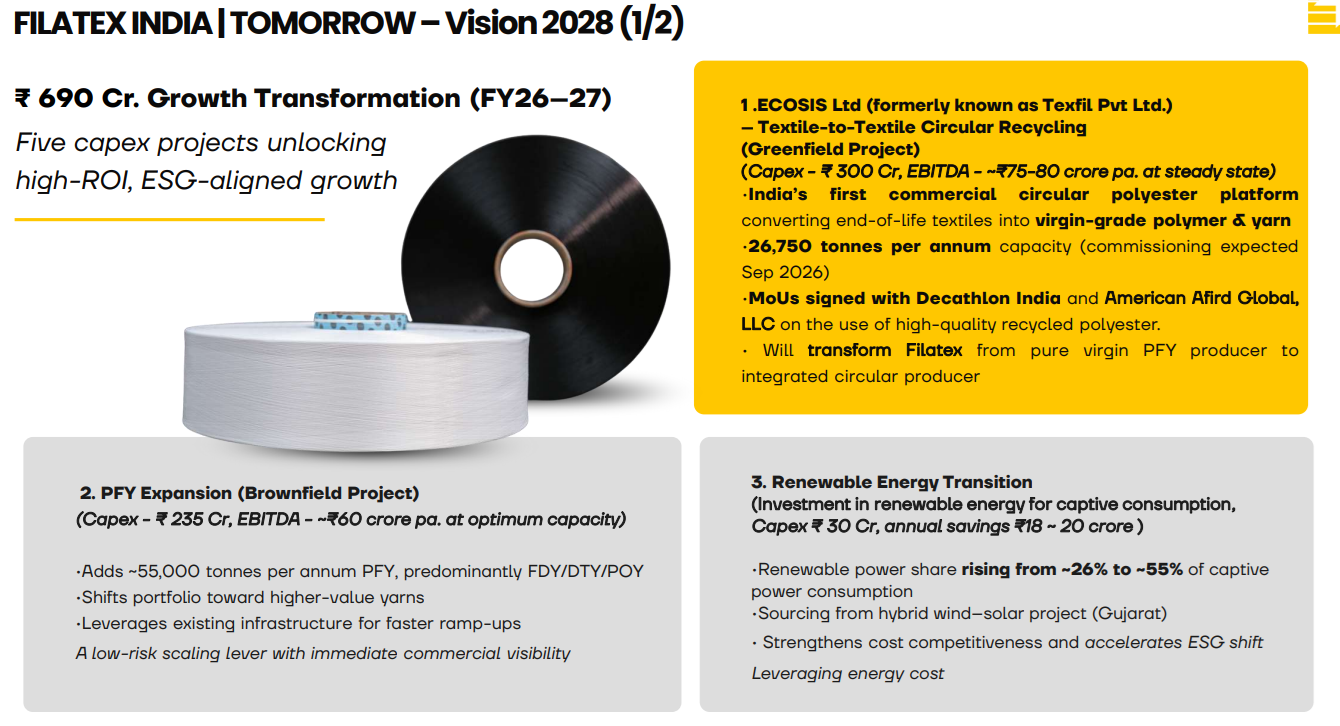

THE BIGGER STORY — ECOSIS

Filatex is building India’s first commercial textile-to-textile chemical recycling plant (26,750 TPA) under its subsidiary ECOSIS, commissioning expected September 2026.

Why it matters:

- Less than 1% of global fibre today comes from textile waste — the opportunity is massive

- MoUs already signed with Decathlon India and American & Efird Global for trials

- Projected EBITDA margins of ~30–35% from recycled PFY vs ~8% from virgin PFY

- India’s textile recycling market alone is projected at USD 3.5 billion by 2030

OTHER CAPEX UNDERWAY (Total: ₹690 Cr)

- PFY brownfield expansion: +55,000 TPA (₹235 Cr)

- Renewable energy: Renewable power share rising from ~26% to ~55% (₹30 Cr)

- Steam monetisation to nearby industries: EBITDA of ₹60–65 Cr at steady state (₹85 Cr)

- Factory automation with Italian tech partner (₹40 Cr, July 2026)

NEAR-TERM HEADWIND

Q4 revenue was ₹985 Cr, down 8.75% YoY due to geopolitical tensions in West Asia that temporarily spiked PTA/MEG input costs. Government has already waived customs duty on these for 3 months from April 2, 2026.

The core business remains intact. The capex story is just getting started.

Not a research subscriber yet?

This is the kind of quarterly tracking we provide for covered stocks.

(opens in new tab)Explore Katalyst Wealth subscriptions →

Hope you found the blog post useful and it added value to your investment decisions. Sign up for more interesting stock ideas and industry notes.

Disclaimer: This is not a recommendation to buy/sell any of the stocks mentioned above. The securities quoted are for illustration only and are not recommendatory.

Ekansh Mittal

Research Analyst

SEBI Research Analyst Registration No. INH100001690

Research Analyst Details

Name: Ekansh Mittal Email Id: (opens in new tab)[email protected] Ph: +91 727 5050062

Details of Associate: Not Applicable

Analyst Certification: The Analyst certify (ies) that the views expressed herein accurately reflect his (their) personal view(s) about the subject security (ies) and issuer(s) and that no part of his (their) compensation was, is or will be directly or indirectly related to the specific recommendation(s) or views contained in this research report.

Disclaimer: (opens in new tab)http://www.

Registered Address – 7, Panch Ratan, 7/128, Swaroop Nagar, Kanpur – 208002

Place of Business – 205, Ratan Floor, 113/120, Swaroop Nagar, Kanpur – 208002

Compliance Officer/Grievance Redressal – Mr. Ekansh Mittal, +91-9818866676, (opens in new tab)info@

“Registration granted by SEBI and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors”.

“Investment in securities market are subject to market risks. Read all the related documents carefully before investing.”

The views expressed are based solely on information available publicly and believed to be true. Investors are advised to independently evaluate the market conditions/risks involved before making any investment decision

This report is for the personal information of the authorized recipient and does not construe to be any investment, legal or taxation advice to you. Ekansh Mittal/Mittal Consulting/Katalyst Wealth is not soliciting any action based upon it. This report is not for public distribution and has been furnished to you solely for your information and should not be reproduced or redistributed to any other person in any form. This document is provided for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision. Ekansh Mittal or any of its affiliates or employees shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. Neither Ekansh Mittal, nor its employees, agents nor representatives shall be liable for any damages whether direct or indirect, incidental, special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information. Ekansh Mittal/Mittal Consulting or any of its affiliates or employees do not provide, at any time, any express or implied warranty of any kind, regarding any matter pertaining to this report, including without limitation the implied warranties of merchantability, fitness for a particular purpose, and non-infringement.

The recipients of this report should rely on their own investigations. Ekansh Mittal/Mittal Consulting and/or its affiliates and/or employees may have interests/ positions, financial or otherwise in the securities mentioned in this report. Mittal Consulting has incorporated adequate disclosures in this document. This should, however, not be treated as endorsement of the views expressed in the report.

We submit that no material disciplinary action has been taken on Ekansh Mittal by any regulatory authority impacting Equity Research Analysis.

Use of Artificial Intelligence: RA may infrequently use Artificial Intelligence (AI) tools like chatgpt, notebooklm, etc. in its research services to enhance the quality and efficiency of the recommendations provided to clients. The tools are primarily used for data collection and generating con-call summaries for the purpose of research.

In accordance with Regulation 24(7) of the SEBI (Research Analyst) Regulations, 2014: We take full responsibility for the security, confidentiality, and integrity of client data used in conjunction with AI tools and we ensure compliance with applicable laws regarding the use of AI tools.

Disclaimer: You can access it here – (opens in new tab)LINK

Whether the research analyst or research entity or his associate or his relative has any financial interest in the subject company/companies and the nature of such financial interest – No

Whether the research analyst or research entity or his associates or his relatives have actual/beneficial ownership of 1% or more securities of the subject company (at the end of the month immediately preceding the date of publication of the research report or date of the public appearance) – No

Whether the research analyst or research entity or his associate or his relative has any other material conflict of interest at the time of publication of the research report or at the time of public appearance – No

Whether it or its associates have received any compensation from the subject company in the past twelve months – No

Whether it or its associates have managed or co-managed public offering of securities for the subject company in the past 12 months – No

Whether it or its associates have received any compensation for investment banking or merchant banking or brokerage services from the subject company in the past 12 months – No

Whether it or its associates have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company in the past 12 months – No

Whether the subject company is or was a client during twelve months preceding the date of distribution of the research report and the types of services provided – No

Whether the research analyst has served as an officer, director or employee of the subject company – No

Whether the research analyst or research entity has been engaged in market making activity for the subject company – No